Berkshire, Buffett, and the Global Portfolio

Any serious investor would’ve spent their weekend reading Buffett’s latest letter. Quoting almost in full from his eulogy to the late, great Charlie Munger:

Nevertheless, Charlie, in 1965, promptly advised me: “Warren, forget about ever buying another company like Berkshire. But now that you control Berkshire, add to it wonderful businesses purchased at fair prices and give up buying fair businesses at wonderful prices. In other words, abandon everything you learned from your hero, Ben Graham. It works but only when practiced at small scale.” With much back-sliding I subsequently followed his instructions. Many years later, Charlie became my partner in running Berkshire and, repeatedly, jerked me back to sanity when my old habits surfaced. Until his death, he continued in this role and together we, along with those who early on invested with us, ended up far better off than Charlie and I had ever dreamed possible. In reality, Charlie was the “architect” of the present Berkshire, and I acted as the “general contractor” to carry out the day-by-day construction of his vision. Charlie never sought to take credit for his role as creator but instead let me take the bows and receive the accolades. In a way his relationship with me was part older brother, part loving father. Even when he knew he was right, he gave me the reins, and when I blundered he never – never –reminded me of my mistake. In the physical world, great buildings are linked to their architect while those who had poured the concrete or installed the windows are soon forgotten. Berkshire has become a great company. Though I have long been in charge of the construction crew; Charlie should forever be credited with being the architect.

And he reiterates what Berkshire looks for in a good company:

We want to own either all or a portion of businesses that enjoy good economics that are fundamental and enduring. Within capitalism, some businesses will flourish for a very long time while others will prove to be sinkholes. It’s harder than you would think to predict which will be the winners and losers. And those who tell you they know the answer are usually either self-delusional or snake-oil salesmen. At Berkshire, we particularly favor the rare enterprise that can deploy additional capital at high returns in the future. Owning only one of these companies – and simply sitting tight – can deliver wealth almost beyond measure. Even heirs to such a holding can – ugh! – sometimes live a lifetime of leisure. We also hope these favored businesses are run by able and trustworthy managers, though that is a more difficult judgment to make, however, and Berkshire has had its share of disappointments.

Those dreaded heirs living lifetimes of leisure! Where is my Northern Italian estate?! Ugh.

My investing career has been a lot shorter than Buffett’s — though it gives me some hope that Munger only started managing money when he was 38, and he was “only” 35 when he first met Buffett. Perhaps there is some hope for us late starters after all.

Anyway, look — I am not going to write you too much about that. You can read the whole letter here. Over time, Berkshire’s compounded annual return is 19.8% — the S&P in the same time period (since 1965) has returned 10.2%. Berkshire trounces over most money managers and is a lot more humble than the majority of them. It’s a model that works.

Changes to our global portfolio

Returns for the global model portfolio so far for the quarter are 7.63% versus. the Vanguard All-World index, which is 4.15%. Let’s start with the mistakes. Obviously these returns are unaudited, gross of any fees, and not financial advice.

Paramount & and the perils of Shari.

Paramount is a very small position (>1%) in the portfolio. We have been selling it in bits and pieces. I’ve written to you a lot about Paramount, and the inherent issues with it. No doubt it possesses a lot of good assets — Paramount Studios, etc, but selling it is fraught with challenges. National Amusements is saddled with debt yet controls 80% of the voting shares. Paramount is loaded up with debt too, and any purchase would put debt covenants into peril. As Buffett said above — “It’s harder than you would think to predict which will be the winners and losers.” —I’m no snake oil salesman.

Manchester United

A reader wrote in the weekend “Manchester…a football franchise…I wouldn’t touch that with a ten foot barge pole” — fair comment, and one worth consideration.

While I think there is a lot of value in sports franchises. There’s a reason why sports franchises have been pursued by so many rich folk — you are buying i) a die-hard fan-base ii) a history that you cannot create from scratch iii) very lucrative sports streaming rights. WBD + DIS + FOX recently announced the creation of “Spulu”, which will control 55% of the sports streaming rights in the US. The problem with Manchester United is the dreadful Glazers, who previously controlled the whole co (again, via a different class of shares). The fact that they sold a partial stake to Jim Ratcliffe and didn’t accept an all-cash offer from the Qataris is borderline negligence. An all-cash offer would’ve awarded shareholders ~$29 a share or so, a handsome premium and a good arbitrage. The actual offer accepted was mostly buying the Glazer’s controlling class of shares and buying a limited number of ordinary shares. We sold the remainder of our position and have cashed out of it. Best of luck to Ratcliffe, but we would’ve preferred an all-cash offer. (On the other hand, the Activison-Blizzard arb we held did go through, which netted us a 26% return in full — you win some, you lose some).

We still have faith in the value of sports franchises — we hold Liberty Media Formula One, which owns the F1 franchise — it’s not often you get to own an entire franchise that covers multiple teams. We also hold Churchill Downs, the company that owns the iconic Kentucky Derby. They have been going since 1875 and don’t seem to be showing any signs of stopping soon.

One final loser — Hong Kong and Shanghai Hotels Ltd (HKSH). They were founded in 1863 and are owned by the venerable Kadoorie family. The Kadoorie’s think in centuries, not quarters, which is why the family has accumulated Rothschild-level wealth. HKSH owns The Peninsula Hotels, which is where the very rich stay when they want to get away from the plebs at the Four Seasons. The company has adroitly grown its assets while utilizing a very conservative balance sheet.

In addition to the hotel business they own a lot of prime property across the world — London, Paris, and of course Hong Kong — they also operate a golf course, a members’ club — things people can’t easily replicate. There is only so much land in Hong Kong. It’s a small place. We continue to hold the stock with a long-term view, much like the company’s majority owners. The company has net tangible assets of ~$35bn HKD and a petite market cap of ~$9bn.

Winners of note —

EXOR, the holding company of the billionaire Agnelli family (are you seeing a theme?), is now trading above the 100 EUR mark. It has gained 11.75% this quarter. Exor owns interests in Ferrari (another company you couldn’t recreate the history of) and Stellantis, which owns Fiat, etc and is the world’s fourth biggest auto maker. It's compounded its NAV at 18.6% per annum since 2009. The holdco also owns Juventus Football Club, CNH Industrial, Christian Louboutin, etc — think of it as a publicly listed family office.

The other holdco situation that was worked out well is Bolloré SE — founded in 1822 (we love an old company). Bolloré is the holding company of Vincent and co, and holds interests in everything from UMG to Vivendi and Canal+ — it also holds some logistics and energy and industrial assets. There is a wonderful (if lengthy) explanation of the exquisite financial engineering of Vincent Bolloré by Andrew Brown of East72 — link here. He explains it better than I could ever. It makes good bedtime reading — I warned you — it’s long, but good. Bolloré has appreciated +10% for the quarter in model portfolio.

Finally, luxury continues to do well for us — LVMH/CDI has appreciated +15% and 12% respectively. Brunello Cucinelli has appreciated +29% for the quarter, a remarkable achievement for a company that I took an interest in because I started wearing my girlfriend’s scarves around Paris. Cucinelli has the same durability as Hermès — an almost fetishistic devotion to quality. You can see the quality in the company’s operating income, which has grown impressively since 2009.

You can watch my gonzo-style assessment of luxury here, while I wear Brunello scarf:

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

Other contributors include Disney, Dominos (US, not ASX), Suntory, Mastercard and Diageo. Mastercard (and its peer, Visa) earns money by taking a small piece of the pie on every transaction made using its network — whether it is via debit card or credit card. Suntory owns Jim Beam, Hibiki, Strong Zero and BOSS coffee. We like it because of the weak yen and the relatively depressed prices of high quality liquor companies. Across the board these companies have sold off — even “royalty” like Pernod-Ricard and Brown-Forman.

A new addition - Nintendo

Nintendo has been a co I’ve watched for a long while — they’re a combination of IP (Super Mario, etc) and platform. It took me time hanging out with people who use their Nintendo Switches constantly to see the value — people love them and they are attached to brand value.

Much like the Barbie movie there’s a lot of value within Nintendo’s universe that’s yet to be unlocked — movies, TV series, etc. There is also the launch of the Switch 2, which is rumored to be announced in June. In spite of being a legacy platform sales of the Switch have continued to grow and grow — it’s impressive. We expect sales of the Switch 2 to follow a similar trajectory.

NZ

Oceania (OCA) — down and dirty at 56c. CEO stepping down — we don’t mind that; a new broom could be good. Trading well below NTA of $1.40…just sayin’

Aus

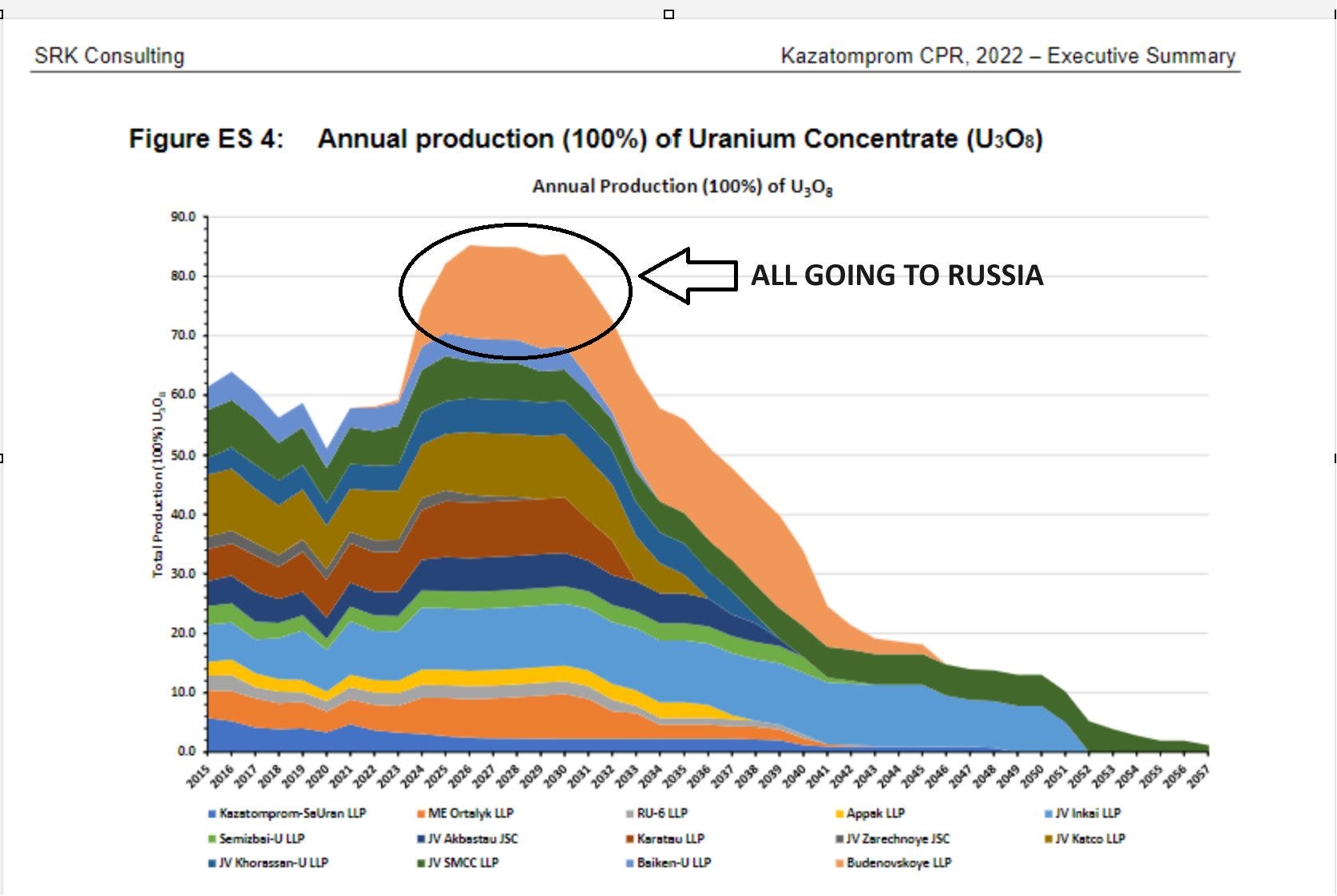

Uranium — sold down ~5%. Supply/demand hasn’t changed. Back up the truck…? Note below — and note the amount Russia is taking over the next few years…that’s supply not going to the west. Slide below is from SRK’s recent Kazatomprom research and accounts just for Russian stock — this is important — Russia supplied the west with about 12% of its uranium supply last year.