Birkin Baby

Louis Louis Fendi Fendi Gucci Gucci Pradaaaaaa

Why we love a Birkin

Hermès — posted 3.36bn euros of revenue for the last three months of 2023, up 17.5% at constant exchange rates from the prior-year period, beating analysts’ expectations of 3.26 billion eur. The company’s operating profit for 2023 increased to 5.65 billion eur from 4.7 billion eur in the previous year, while net profit jumped 28% to 4.31bn eur. We love all this — the way the Hermès machine works is that clients need to buy several things before they even get offered a Birkin. The classic old machine of perceived shortage of supply. And the ultimate way to wear a Birkin? Treat it like something you bought from the mall, or from Strand Bags — affix it with stickers like its namesake, Jane Birkin. That’s the real flex.

Anyway — continue to be believers in LVMH, Hermès, Richemont and Brunello Cucinelli. We’re less certain on the others — Kering had a weak showing at the recent fashion weeks (Gucci who??) while the smaller houses suffer from economics that lack the “machine” of scale. Don’t get me wrong — the recent showing of Prada and Miu Miu was a masterclass in design, but Prada lacks the “killer product” of a Cartier love bracelet or a Birkin. And you either need to be big, or have killer product.

A nice man who drives tractors or something was asking me “what's the value in handbags?” and here’s your answer below — that's the value — you could also just ask your girlfriend or wife if she would like a Birkin, and you’d get a similar answer.

NZ/AUS

A lot of results to get through today — first of all AoFrio, which continues to disappoint. Revenue came in -10% from pcp to $66.6mn, while pre-tax loss increased to $3.3mn. Lots of mention of “prevailing macroeconomic conditions” (where we’ve seen record profits in the States and elsewhere, everyone in NZ seems to be in a parallel universe).

IoT segment sat relatively flat at $35.1mn, while the motors segment declined almost 17% — no surprises there, it’s a melting ice cube that funds the growth of the IoT segment. Therein lies the problem — the IoT segment hasn't grown. Management is guiding $70-80mn for FY24. On the other hand, nice to see some positive cash flow ($3.9mn).

We still like the core product and think it is undervalued — but disappointing results. Ideally we’d like to see a larger player buy AOF as a “bolt-on” acquisition — it's not served well by the NZX — too small to be included in the indexes, and very low liquidity. Waiting for a Prince Charming to come along…there’s too much “next year will be better”. Management should be, at this point, engaging M&A advisors as how best to hock off the company, because it’s had a long time on the stock exchange to prove itself and it hasn’t. I am addressing this directly to the CEO and directors — it’s a question incumbent upon them at this point.

The main question I have is: why is AoFrio still on the stock exchange? It would be better elsewhere (a la MHM Automation).

Stronger result from Channel Infrastructure, which delivered EBITDA of $87.2mn — strong fuel volumes drove growth, which are now approaching pre-Covid volumes (c.92%). We expect this trend to continue as international and domestic flights continue to be in high demand. A “toll booth” on fuel needing to be stored in NZ — trading at 6% free cash flow yield!

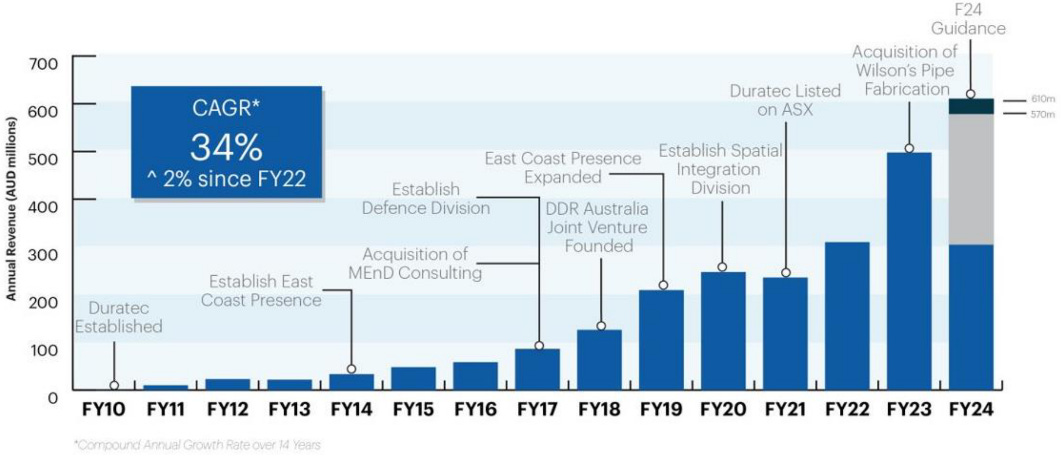

Duratec — has been on a wild ride this past week, dropping from $1.44 to $1.21 within the day (!) and then back to the $1.30 zone. Results were as expected — pipeline of $3.7bn and cash on hand of $58mn. Wasn’t a blockbuster result, but was clearly a market overreaction…

Speaking of …DGL — precarious drop from $1.00 to 60c in a day (!). Stock has made a good recovery — at 70c today. Stock was oversold in spite of delivering a record profit 1 per cent above its guidance of $65 million in underlying earnings. Obviously growth is not going to be as spectacular as previously reported. Same deal as DUR — serial acquirers are inherently impeded by the pond they fish in. Plenty of growth ahead though, we think…

Media stocks (i.e. the beguiled three) or: is the force strong in David Zaslav?

Results from the three legacy media outfits are out — DIS, PARA, and WBD. We reported on Disney here - quick refresher, good results ($1.22 vs 99c expected) and recent deals with the exclusive streaming of Taylor Swift’s “Eras” tour, Spulu (sports streaming service with ESPN, Fox and WBD).

WarnerBrothersDiscovery fared worse — RIP Newshub, the most recent victim of Zaz’s cuts at the debt-laden Frankenstein of a network. John Malone, effectively Zaz’s shadow boss, used to be known as the “Darth Vader of Cable” (I wish WBD owned the Star Wars franchise, but please enjoy the above meme regardless). Perhaps Zaz is the Kylo Ren of streaming?! It’s a sad day for NZ news — But hardly surprised to see the brutal cuts reach the NZ. Imagine Zaz, dwelling in his newly purchased Californian pied a tere (he paid a cool $16mn for it) which was formerly home to the late Bob Evans, who produced The Godfather, Chinatown and Rosemary’s Baby.

“New Zealand, where’s that?” Zaz might ask. I mean — he should know, WBD owns New Line Cinema, the co that produced LOTR. Zaz — just think “Hobbits”.

Anyway, the late Bob Evans’ magic clearly hasn’t been passed onto Zaz, which saw basically a shitshow of bad results — revenues decreased 7% to $10.8bn, and while the sizeable debt load was reduced (sorry, Newshub) by $1.2bn and net leverage fell below 4x to 3.9x — but that 30% decline in adjusted earnings for the studio doesn’t look good either way you cut it. “Barbie” was a big hit, but “Aquaman” was a flop. More disappointingly, Max (the company’s ineptly named streaming service) saw mediocre subscriber growth — 97.7mn from 96.9mn pcp. That’s deeply unimpressive when you compare it to Netflix’s growth of 13.1mn subscribers for the same period. Adding salt to the wound is near-constant misses of adjusted EBITDA — adjusting it down aren’t the adjustments we were looking for!

The stock is trading around all-time lows. We suspect the only reason it isn’t being circled by activists is because of who the majority shareholders are — John Malone, the Conde Nast family, etc. Malone has famously complicated capital structures — the Liberty series of companies (Formula One, Sirius XM, etc) all are tracking stocks. WBD is basically debt with an equity stub (I.e a leveraged buyout). Paying down debt is one thing, but you need to beat those EBITDA expectations as well for the stock to work. I suspect, strongly, that the powers that be will retain Zaz for as long as he retains the role of hatchet man for the Wizards of Oz. Eventually they’ll need someone with creative direction.

More woe at Paramount — $7.6bn in revenue for the last three months of 2023, down from $8.1 billion in the year-earlier period. The company lost 2 cents per share in the fourth quarter, versus an 8-cent profit a year earlier and the analyst consensus forecast of a 1-cent loss. Some good news in the streaming segment — revenue surged 34% to $1.9bn, and ~11mn new streaming subscribers (compare that to WBD!)

Again, there’s value there — 67.5mn subscribers ain’t nothing to sneeze at! But same sitch as WBD — a whole lotta assets and a whole lot of complicated debt. Can somebody just buy the whole thing? David Ellison, you reading this?

My point is — these stocks are cheap and their IP has a lot of value. But finding any deal (and I bet Shari’s banker Byron Trott is trying his damn hardest) to catalyse that value is going to be hard.

Who wants to buy Refinery29?

This is extremely niche but a long time ago yours truly wrote a popular fashion blog that parodied a famous designer — it was my intro to the wild world of the internet. Refinery29 was a “lifestyle” website that the girlies would read. At its peak - in 2019 (oh the 10’s, how I miss you) — the site and “brand” was sold for $400mn. Anyway, Vice paid that much and now Vice has shut down, an event more or less predicted by Kenny Roy’s shut down of the fictional Vaulter in Succession. Vice was once hailed as the new media — they had a TV channel, YouTube, site, blog, etc — they were making documentaries and made Action Bronson famous. They did a lot!

Anyway, now media is “dead” (Newshub, etc), and Fortress, which owns the remnants of Vice, is keen to sell Refinery29 for $30mn. I mean, who wants to buy it at that price? Who wants to buy Newshub?? Does anyone?