Board Rolls, Spark, and Dark Factories

Rollin' down the river

Brown-Forman — Stock at $35.77… up 15.00% on the month. Remember when everyone said “oooh Eden why do you like booze stocks?” And now the bottom is falling out of the Mag 7, a lot of these stocks are starting to re-rate. There’s still stragglers — Remy Cointreau at 45.62 EUR … trading at 1.25x price/book — it hasn’t traded at this multiple since 2010 — obviously there is a current ebb in consumer habits towards Cognac — cyclical. Plenty of people drink Jack, made by Brown-Forman…damn straight!

Rakon — Now at 52c, below NTA of 55c! Nice to see a strong director appointment — John Raby (ex-ASB CFO). The company has a long way to go to win back market confidence…

Bremworth — Board roll. George Adams has stepped down as chair and Rob Hewett is the new chair. Quite an orderly transition of power, don’t you think? As I’ve said before — I think Bremworth ought to sell to one of the parties that have expressed interest in it — it has a big pile of cash from the insurance settlement, and I think the company is too small on its own to ever be that efficient. Rather see it sold with a strong balance sheet to a larger player.

I say orderly transition of power because I’m thinking of the current stoush at NZME — Grenon almost certainly was +50% support from shareholders, including Spheria, who own 19% of the company. So I read this interview with current Chair Barbara Chapman with interest — some choice quotes:

Chapman, speaking about Grenon’s proposal, said the NZME board had concerns about governance, editorial independence and board nominee suitability, although she would not elaborate on the latter.

“I won’t go into the nominees today. We’re still doing some assessment of who they are and what skills they bring.”

However, she believes NZME’s future could be undermined by a major change of directors and direction.

She said it was “time for the board to insert itself into the discussion”, particularly, she said, on the financial performance of the company, “because what’s in the public domain is wrong”.

I am not sure what Chapman thinks is “wrong” with the discussion of the financial performance of the company in the public domain. In 2022, Operating NPAT was ~$23mn, while in 2024 it was ~$12mn. That’s fact — and very much in the public domain.

Oh, wait, here’s Chapman explaining what she means:

A few years ago when this board was formed, this was a struggling company with really high debt and it was on shaky grounds

That’s true, but I think what the “public domain” may be interpreting is the precipitous decline in Operating NPAT.

It’s also worth noting Chapman’s discussion of director nominees — “we’re still doing some assessment of who they are and what skills they bring…” is a strange statement, as if the current board are in a position to pick the new directors — the issue here, of course, is that if Grenon has 50% or more support from shareholders he can simply roll the entire board.

Here’s the kicker — the bit that really makes you go, eh?! It refers to the 17-page letter Grenon sent NZME’s board:

NZME has so far declined to release the letter, which is understood to cover governance, financial, operational and editorial concerns and matters.

“I’m not going to go into it because we’ve got to honour the shareholder’s request and that’s to send it out with the notice of meeting as a supplementary paper, so we will do that,” said Chapman.

Grenon said in his statement on Sunday: “I am not restricting NZME from releasing the document. They are doing that on their own.”

All of this to say — kudos to Bremworth for facilitating an orderly transition of power, and big question marks for the NZME board who, much like the previous Fletcher board (of which Chapman previously chaired), seem to exist in a space of ivory towers and Directors-Institute-approved-jargon.

Moving to Spark now — looked like it would go sub-$2.00 y’day — for those keeping track at home, that’s a -57% drop in the last 52 weeks. Not that long ago Spark was thought of as a stable dividend stock your granny might have. Now it is trading more like — I don’t know — AllBirds?! I’m not even joking:

I mean, it’s hard to know what Spark is thinking — here’s a bizarre advert I found on TikTok last night:

What does it mean?! Why does it look like this?! Did someone see a rap video from the mid-2000s and go “oh yeah, that’s what the kids want. Get that on the TikToks”.

To really reinforce the point — Spark’s market capitalisation was $9.3bn in 2023. Now it is $3.83bn. And to be really blunt — it’s very unusual that CEO Jolie Hodson remains in her job while she has seen the market capitalisation of her company shrink so alarmingly — to put it another way, since 2023 +$5.47bn of shareholder value has been eroded.

If you go back since the beginning of Hodson’s tenure, in 2019, it doesn’t look much better — revenue then was $3.51bn. It’s now $3.75bn. That’s hardly inspiring. If anything, it’s treading water.

I am watching Spark with interest — it seems like a case of poor management. If you like, email me with any thoughts or insights — curious to know more about the precipitous decline of a once-boring dividend stock.

Overseas

Overheard in an airport lounge, somewhere — “The dark factory…20k jobs gone…all AI, no workers. We’re moving our stuff to Indo.”

What is the dark factory, you ask? Here’s Xiaomi’s new “dark factory” —

No humans. All automated (with AI). It operates in the dark. The machines do not take breaks. It produces one smart phone every second.

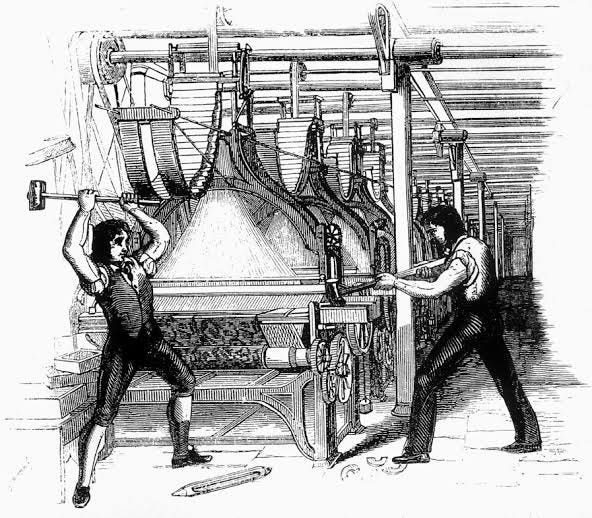

If you will for a moment, imagine a future where all of China’s six million factories are automated. China has a ~112mn-strong manufacturing workforce. There’s a lot of potential unemployment China has to think about — I mean, I guess, they can do what the US did and become a service-based economy? But in the short term, if that were to happen — then I wonder if it’s akin to the luddites at the start of the Industrial Revolution. I wrote this in my internal notes earlier, on AI and the Industrial Revolution:

The book “Engines that Move Markets” remains the best book on investing in the tech economy. It posits that bubbles are a function of markets, and what they do is spread technology and infrastructure very fast. Consider the railroad bubble of the 1800s. All over England railroads were built with gusto. Many railroad companies were listed, and their stock -- in the parlance of Wall Street Bets -- “went to the moon”. Of course most of their stock crashed eventually, and investors lost enormous amounts of capital. But all was not lost! All that capital went somewhere (as Marx tells us) -- it went into building railways, and stoking the Industrial Revolution.

I wonder if the same thing will happen again with AI (“history doesn’t repeat, but it rhymes”). Enormous amounts of capital is being poured into developing it, into data centres and power plants and so on. I fear most of this capital will be lost into an explosion of excess, as it has happened in the past -- the same happened during the dot com bubble (and the telecom bubble, and the bicycle bubble, and so on -- our history is full of “rhymes”, if not “repeats”). It is no doubt a technical advance, much like the railways and the Industrial Revolution were for the 19th century. My mind now turns to the Luddites of the 19th century -- the men and women who destroyed machinery in protest, as their jobs were being taken. There are luddites in every revolution -- many of the jobs of the 19th century do not exist anymore. Wikipedia lists +184 occupations that no longer exist throughout humanity’s time, and I am sure this is merely scraping the surface.

As we know from history, most of the time the Luddites lose out. Technology’s progress is inevitable, and one would be foolish to ignore its steady march. Currently, we are laying the metaphorical “railway tracks” across the world -- once those tracks are laid, I suspect they will be here for the long run.

I don’t see any reason to change this perspective. If dark factories are the future of China, then it’s no wonder the Chinese government are pumping in stimulus…