De.mem reaches cashflow positive; Arnault is bullish on the US

But they still sold less Cognac

NZ

Noting IFT fell some on Deepseek’s AI model — IFT has a large investment in data centres, and this may be misplaced if Deepseek can do the same thing as ChatGPT on a much smaller CapEx investment. IFT has been a great growth story, but I suspect the data centres will continue to weigh upon the company…yours truly quoted in BD:

“Now there’s a big question mark hanging over exactly how well they will do for the company. With much more efficient models from DeepSeek, you’re going to see a lower capital expenditure spent on datacentres. "Why use a massive shed when you can do it on a shoestring and a much smaller space?” He said he expected investors to move out of Infratil and CDC on the back of the selloff. “Datacentres were hot. Until they weren’t.”

ASX

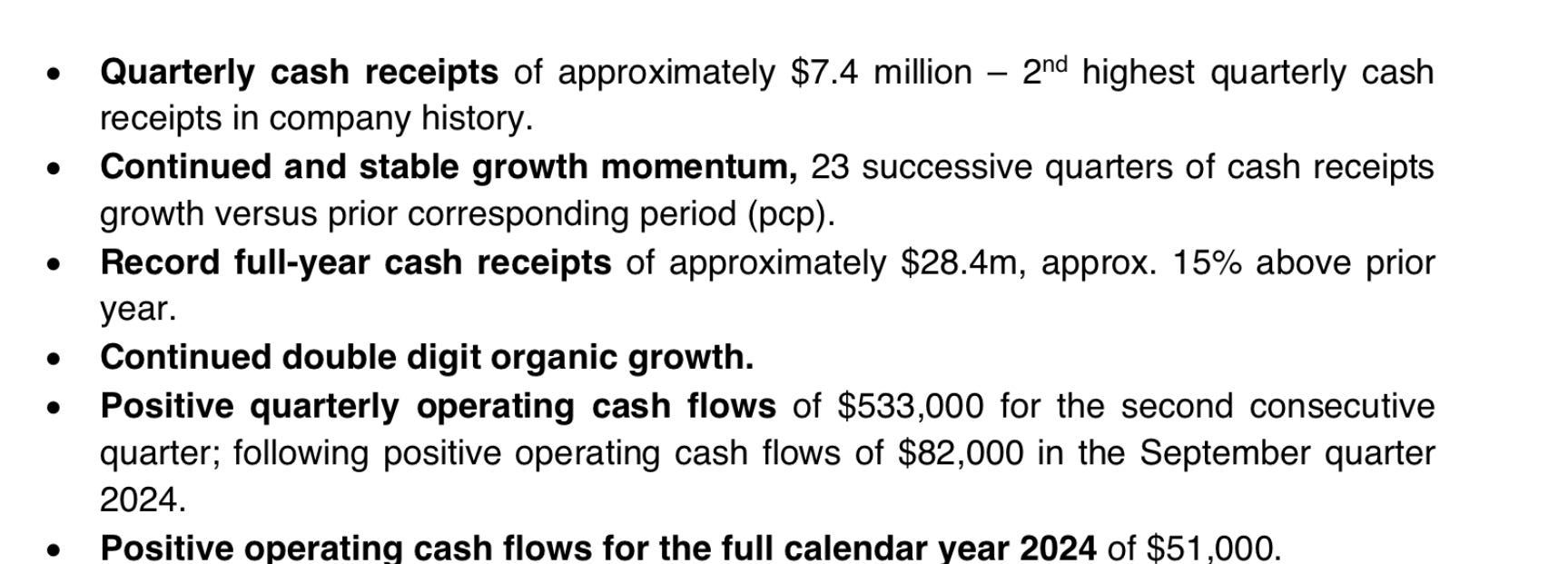

DEM — We released a report on De.mem, the Australian water treatment company, all the way back in May. Link. Key aspects to the thesis were heading towards cashflow positive & prudent management of their strategy … slow and steady wins the race. Stoked to see they’ve reached cashflow positive, while cash receipts continue to grow, reflecting the SaaS-like qualities of their products — see below:

Stock at 14c as of writing.

Chemist Warehouse — This thing is listing soon. Sales just topped $5bn. It’s a Goliath, but I just pause at the valuation — if everyone’s lining up to buy stock, you’re not going to get a bargain.

Overseas

LVMH — Weaker results (the main thing for me is margin contraction — watches and jewellery for instance shrunk from 19.8% to 14.6%), while lower end offerings like Sephora provided a rarer bright spot — sales jumped from 17.8bn to 18.2bn. A mostly flat year, though obviously booze is weak (and this is priced into the stock…). Noting main weakness comes from Cognac — we’ve seen similar weakness over at Remy.

Good news, though — FCF sitting at $10.4bn. LVMH is still a cashflow machine, and that’s what you write home to mum about.

I keep thinking about where to from here with luxury — we’ve had really good results from Brunello and Richemont, and while LVMH’s results aren’t bad they’re not getting me all that excited, either. I watched Chanel’s haute couture show this morning — see the pop star Dua Lipa below — and new designer Blazy’s clothes reflected a mature and yet playful ethos — they’re clothes you want to wear, but you can also dream in. Chanel is privately owned, of course, but it acts as a bellwether for the wider industry — the question we need to ask when looking at LVMH is what does it look like in two years time.

If Chanel’s collection is anything to go by, the industry seems to be embracing a period of cautious hope. As mentioned, we saw good results from both Brunello and Richemont (both have faster moving inventories). Given this, I think there’s some hope that luxury sales will pick up going forward — it takes a bigger push for a ten-ton elephant like LVMH, of course, but you’re rewarded with cash flow.

Dissecting Arnault’s earnings call

Worth quoting Arnault in full here (from the earnings call):

As for China, I believe that the Chinese government is now aware of the fact that they need to kick-start the economy. The economy needs to recover, and therefore a few plans have been announced to just help the economy. That's the first thing. The second thing, our high-quality products are still extremely desirable in China. People still want to buy our products. The environment was severely impacted by COVID, then there was a strong recovery, followed by another crisis, the real estate crisis, so it's going to take some time. What I expect is to see a gradual recovery. So we're going to get back to a normal situation after two years. It's not going to happen overnight. In the U.S., it's going to be a boom. But it's going to take more time for China to recover fully.

As for investments, when you look at revenue, well, it's just the end of January, it's not the end of H1, but still we are still investing, we're still communicating, we organize fashion shows, we have a lot of projects to keep this momentum. And I forgot what your third question was. It was about Wine & Spirits? Yes. No, divestment is not on the agenda.

Plenty of gold there — no divestment of MH (as has been speculated); predicting a boom for the US, and stating the Chinese government are engaging on stimmy (we knew this already, but there you go). In fact, Arnault is extremely optimistic on the US:

Back from the U.S., as you've kindly mentioned, I saw the momentum of optimism in the country. After having spent a few days in the U.S., you come back to France, and it's a little bit of a shock. It looks like, in the U.S., people are welcoming you with open arms. Taxes are going to go down to 15%. The workshops that we can build in the U.S. are subsidized in quite a few states, and the American President encourages this practice. The market is developing fast.

Just look at the new store that Pietro opened in New York. It is an outstanding success. The lines are 100 meters long.

If we’re to take this at face value, Arnault seems to be suggesting 1) more production in the US and 2) more share of LVMH’s revenue mix to the US (reasons to be cheerful).

Finally, I think it’s worth thinking about LVMH’s expansion into experiential luxury — with their luxury hotels and trains —

We're pleased to see that we started from scratch 10 years ago. Cheval Blanc was launched in Courchevel, and I think nowadays, everyone, everywhere tells me and rankings confirm that, that this is the highest, the luxury chain in the world, five-star hotels. Not bad for something started 10 years ago. Meaning that we will invest as much as we can in that business, nor does it mean that they are as profitable as Vuitton or Dior or Bulgari, but it does mean that our clients can get a room, experience a stay, take the Orient Express in a slightly privileged environment. It's very much the same environment, as you said. It's experience-based luxury, and not just product-based luxury.

I have long argued that luxury is an experience, rather than a product. You can order most luxury products online, but the quality of the experience is limited to some nice packaging when it’s delivered. Going to a store, being looked after, and having a glass of champagne — that is an experience.

Going back to my first question: where will LVMH be in two years? I still expect some tight margins, but I wouldn’t be surprised to see the company push further into the US while seeing some China recovery (remember y’day — everyone over there is bullish on it…esp HK). Dangers to this thesis include: 1) oversoaking the market in too much stock (see: Kering), 2) not enough superstar designers (there’s still the large "question mark” hovering over where Galliano goes…).

How low can Cognac go?

The big thing overshadowing booze is, of course, Cognac. 3.1bn yr previous to 2.6bn this year. Oof. Of course that includes other spirits as well, but the lion’s share is Cognac. More work to be done, and frankly I’m not sure if Cognac will ever recover to pre-China tariff levels. So MH (and Remy) need to think carefully about how the reposition.

Tech earnings tomorrow

Meta, Microsoft and Tesla all report tomorrow. Expecting a lot of volatility given Deepseek. Tesla has always been overvalued, while I think Microsoft is due for a correction given i) its massive investment in OpenAI and ii) its reliance on increasing Office365 prices to increase revenue.

Switch 2 & Japan

I find it useful to think of how management deploys retained earnings, which of course Buffett talks about endlessly. Retained earnings are simply what is left after everybody has been paid, dividends have been issued, and buybacks have been done. The question is -- what value has been created for every dollar retained? This is not a cut-and-dry answer, because things like R&D and marketing are investments (consider the investment LVMH made into the Olympic games, or Malboro’s iconic sponsorship of Ferrari). You can roughly look at a company and go -- well, over time, has $1 of retained earnings added $1 to market value? This is more art than science -- if you were to say that Amazon’s investment into infrastructure and data centres was going to be a wise investment early on, you’d likely be laughed out of the office. This is why we place so much weight on manager competency -- an exceptional manager can allocate well towards the future, without worrying about the next quarter. The results speak for themselves, as those “seeds” eventually grow into trees.

And therein lies the problem with Japanese companies -- holding retained earnings as cash and not reinvesting them in any way is a little like playing golf against Tiger Woods while blindfolded and enebriated. You’re handicapped in a big way. This is the big reason many Japanese companies lull around, like well-fed carp, and why they often struggle to compete on the world stage.

There’s opportunity here. This first is what we’ve seen last year with Canada’s Couche-Tard (translates to “night owl”) offering $47 billion or so for Japan’s 7/11 chain of convenience stores. Translation: overseas players see opportunity buying these Japanese companies, and Japan’s boards need to seriously consider such offers (especially when they trade at a premium). While Japan is one of the hardest countries in the road to make inroads to, I expect cashed up funds will head over there to find yield -- especially with US companies priced at exceptionally high multiples.

The second opportunity is found within Japan’s few exceptionally run companies. Consider Nintendo. Nintendo is over a century old, and began as a card game manufacturer. Over its recent past it has innovated both IP (Super Mario, Zelda…) and consistently delightful experiences for the consumer. The first Switch console sold +100mn units, which means 100mn+ possible sales of one of their games. In the case of Mario Kart 8, that means about 66mn sales. It’s a big -- and dedicated -- user base.

The Switch 2 comes out this year. Remarkably, it uses hardware compared to last generation’s consoles -- this is typical of Nintendo, who tend to squeeze the best performance out of already very available technology (it also reduces costs). If the Switch 2 performs anything like the first Switch, Nintendo can expect a windfall. The amazing thing with Nintendo is they can sell an 8 year old game -- Mario Kart -- and re-sell it all over again. It’s a wonderful business model, and I’m quite optimistic on the stock. I think of it as the Disney of video games. Could be an interesting stock to own...

More asset sales at Diageo, and Estée Lauder

I’ve written on speculation that Diageo will float and list Guinness, which the company has denied. Now the company is selling its stake in Guinness Ghana for $81mn. This is par for the course — Diageo has been cleaning up their stakes in Africa for some time. But it does raise the point — does this clear the way for Diageo to list a “clean” Guinness, where their stake is 100%? I think there is a strong likelihood this occurs (despite the company’s denials to that effect). CEO Deb Crew needs a win, and this is an easy win.

Also noting Estée Lauder, our favourite embattled beauty company, looking at selling some of its brands. Short term this is a negative for the company, as they overpaid for many brands as they went on an acquisition spree during the 2010s. Long term it’s a smart move to rationalise (I hate that word!) and focus the company.