Don't discount the discount trade

Also: The Beyoncé whisky, free cash flow yields, and Bronfman's Paramount bid

A new week, and my daily reminder that I will be there at the Rakon shareholder’s meeting on Wednesday at 10.30am. See ya’ll there. Also of note this week —DGL earnings, Droneshield, Wesfarmers, NextDC…no, nobody cares about Droneshield’s earnings (it’s a meme stock, it gets the people going!) but the call should be interesting re future pipeline. DGL appears oversold to my weary eyes, but perhaps I need a new eye test.

Other observations — I went to Henderson in the weekend, an exotic locale out west. The Chemist Warehouse was pumping (no, I don’t see the Sigma/Chem Warehouse deal getting past Aussie regulators), while Kmart was so busy I was overstimulated and needed a Kinder Surprise afterwards. I was also taken aback by Reduced to Clear (pumping) — they sell near-expiration products (want some hot sauce, 2 for $6?). It gave off Costco vibes. I love Costco. I enjoyed this interview with Sean Hills, the founder of Reduced to Clear. Suffice to say it was an excellent adventure to Henderson. And the larger point — the discount trade is still in play — people are looking for bargains and they are trading down.

A few “discount trade” ideas

Bottom of the barrel — You can get Dollar Tree and Dollar General at five year lows (both companies are there for a reason…Dollar General specifically has a lot of fixing up to do…but you know, we’re value investors)

Fast food feeders — McDonald’s has done very well since last time I wrote it up, but you could buy Yum Brands (KFC, Taco Bell, etc) at 24x earnings. The Starbucks train has bolted… still like it, but you know, plenty to prove there…

Buy The Warehouse — This trade idea is only appropriate for Sir Stephen Tindall. If you are not Sir Stephen don’t do it. ❌❌❌

Also, yours truly went on Trading Nut’s podcast last week — we talked about Starbucks, Nike, the peso-yen trade, and more. Was a pleasure.

NZ

Noting new interim CFO for RAK. Also Nick Pudney as head of operations and transformation — he previously led the project at Mercury to incorporate Trustpower’s retail assets. One can only speculate what he’s been hired to do here — the optimist in me hopes he is preparing the company to be sold and “integrated” elsewhere!

Summerset — +3% underlying profit up to $89.9mn for the half year — impressive given a soft market. With Arvida out of the running (other than a light arb play) I like Oceania still with Summerset as a “quality” pick.

Fletchers — Around $3.00 it is almost tempted to nibble at. Am I addled in the brain? Lower interest rates > more build activity > priced in lawsuit + impairments given its awful run.

Vista — Potentia, the private equity shop, now owns +18% of Vista, the cinema technology provider. Just saying.

Australia

Nibbling at DGL at 54c…Les Patterson salutes you…

Also (highly speculative) nibbling on Titomic (TTT.ASX) at 16c… has markings of an early Droneshield.

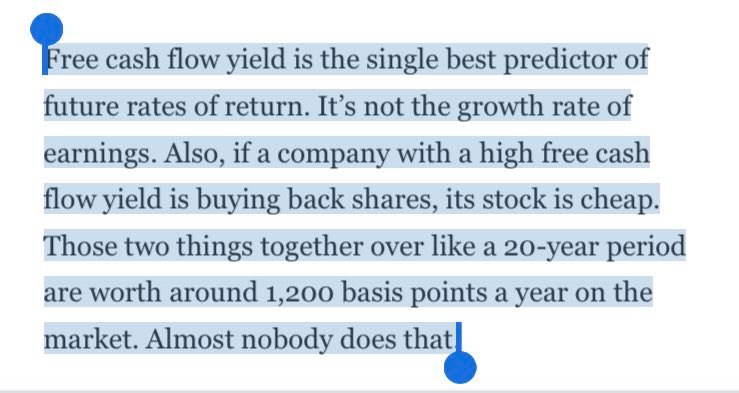

Bill Miller and free cash flow yield…

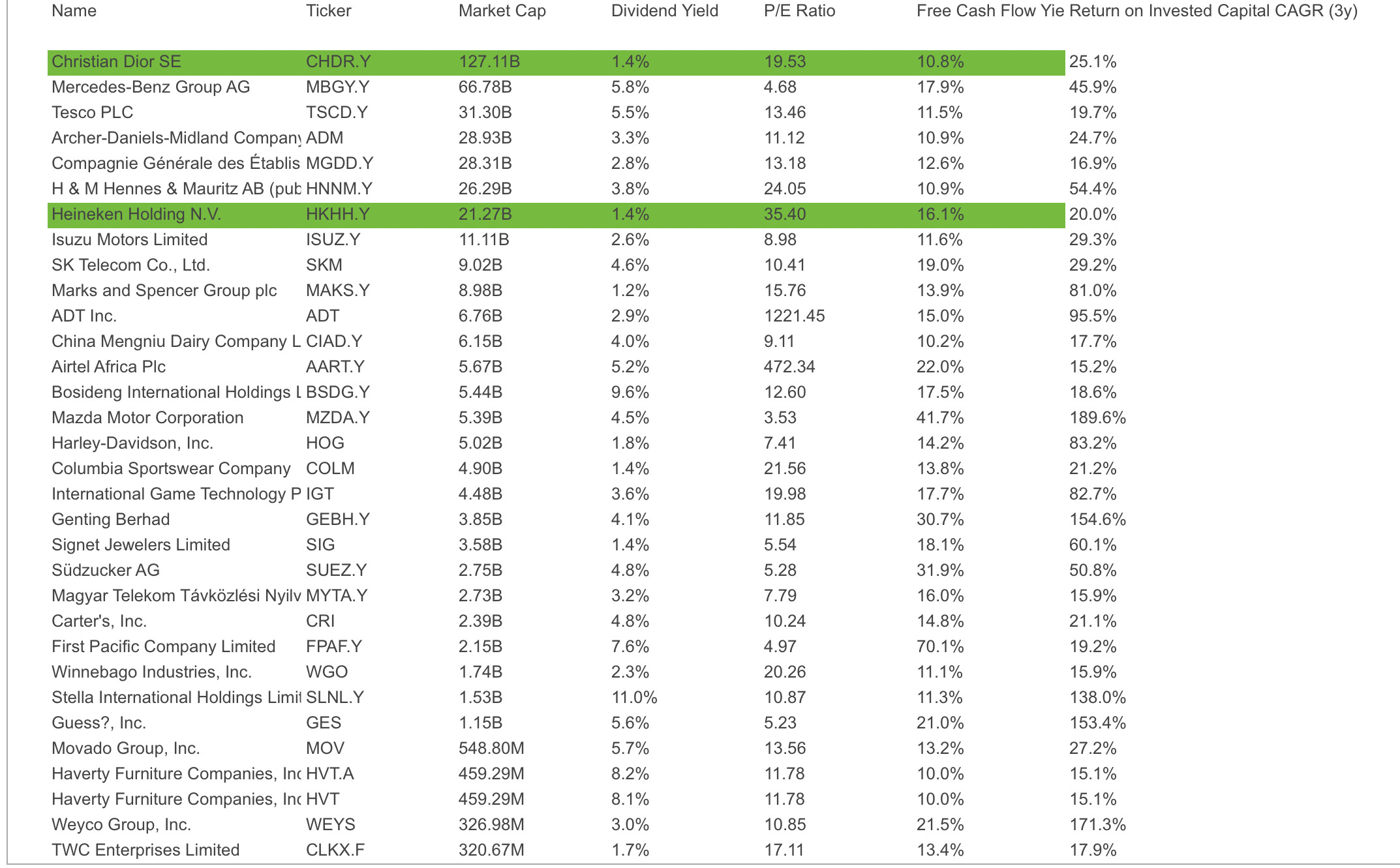

Bobbing for apples… a screen of companies trading at +10% free cash flow yield:

You always make money when companies trade at a double-digit FCF yield (except when you don’t). We already hold CDI (the Arnault’s holding company that holds LVMH) in our model portfolio. I’m loathe to own a beer company versus a spirits company (margins are much tighter) but Heineken could perhaps be worth a look. For the brave: Tesco (Buffett was burnt there once before). I did a survey of the office and nobody wants to buy a Harley Davidson (everyone in the office is under 60 — but still, surely value in the IP?)

Obviously, the no-brainer is CDI. You buy LVMH at a discount to LVMH’s stock price. It’s a nice, simple trade. Luxury will likely decline in the short-term (we’re in a recession, folks). In the long-term luxury will do just fine. I read an interesting paper from CS a while ago where beer companies were their preference — predicting a HOT European summer. Could be a goer.

CDI Adjacent — The Beyoncé whisky

I don’t like Beyonce’s music (I mean, I like 7/11, but who doesn’t?). Beyoncé has a new whisky out, which is made in collaboration with Arnault-controlled Moët-Hennessy. It is called SirDavis. It’s won some awards and was named after Beyonce’s great-grandfather, Davis Hogue, who was a moonshiner.

I have been talking your ear off about the value inherent in the major liquor makers for a while now. They’re all trading well off their historical P/E ratios. I had to sit thinking about the Beyoncé whisky for a while — what it means for spirits and what it means as “a celebrity liquor”. In a way I think this feels lightly positive for the industry — trends towards sobriety and zero alcohol have led to stagnant sales for a while — this feels like a move towards a vibe shift (let’s say, perhaps, that the vibe shift began with Charli XCX’s “brat” — a celebration of living messy and a rejection of clean-living self-sanctimoniousness). Alcohol, like everything, is cyclical — I don’t have any hard numbers (it’s all vibes, man!) but this feels like a shift…

On the Bronfman Bid —

Remember Edgar Bronfman Jr, the original nepo baby? When we last spoke he was wanting to buy Shari Redstone’s Paramount for $6bn or so. It’s not a good deal for a lot of reasons — but add Bill Cohan’s list of co-investors to the mix (if you’re not reading Bill’s newsletter, Dry Powder, what are you doing with your life?).

Other supposed Bronfman investors include a guy named Keith Frankel, an operating partner at MidOcean Partners, the buyout firm, for $1 billion; Simon Falic, the billionaire owner of a group of duty-free shops (and a close friend of Benjamin Netanyahu), for $600 million; Alan Mruvka, a founder of the E! Entertainment channel, for $250 million; Brian Koo, a scion of the LG Electronics dynasty, for $300 million; John Paul DeJoria, the founder of Paul Mitchell hair products, for $600 million; Stephen Paul, the Hollywood producer, for $100 million; and Richard Tsai, the Taiwanese billionaire, for $500 million. Frankly, I don’t see how an investor group composed of this many foreigners can end up controlling CBS. That’s a question I’d like to hear an answer to from Bronfman’s advisors at Perella Weinberg, UBS, Rockefeller Capital, and Skadden Arps

You might think maybe Bronfman had a Big Party and asked everyone if they’d like to pitch in and buy an ageing entertainment asset, and you’d be right, I guess? I like to imagine him calling up the dude who founded E! And being like — hey, do you want to buy Paramount?

This is also why I think the bid is likely to fail — there’s too many parties, too many foreign parties that will attract FTC scrutiny, too many moving parts and frankly, the Ellison deal just makes more sense for everyone involved — Shari gets some cash, her long-suffering banker Byron Trott gets paid, and RedBird, Ellison’s company, gets to own something much bigger than itself. Hooray.