Goodwill Hunting at Woolworths | Netflix takes the cake

plus: RAK, US Earnings, NZL...

Goodwill Hunting

Woolworths — slashing the goodwill value of its NZ supermarkets from $2.3bn by a whopping $1.6bn — the resulting value will be $700mn — and a lot of whingeing from a co that charges a million dollars for a carton of eggs. “Weak medium-term outlook”, high interest rates and “time lag” for new initiatives. We have little sympathy for a supermarket chain that has continuously denied to be price gouging and taking advantage of a duopoly situation. Crocodiles tears…

The Aussie supermarket giant slashed the non-cash value of the NZ supermarkets they bought from Progressive in 2005. It’s a big write-down in value and management “only” attributes a decline of $13mn of its actual earnings for the first half of this economic year to its foolish rebranding of all Countdowns to Woolworths. The rest of its 42% decline in expected earnings before interest and tax is cash — i.e. if we strip out the $13mn rebranding costs, EBIT sits more like $90mn, which is still a drop, but not as precipitous!

Rebranding all the Countdowns in NZ to Woolworths is probably one of the most foolish ideas I’ve heard in a while — no doubt it came from someone with nothing better to do in the C-Suite or from one of those consulting firms that are very good at charging high fees. Now, the that fact that $13mn in real costs have been attributed to EBIT yet goodwill has been slashed like its a victim of the Texas Chainsaw Massacre — that does give us pause. Anyway, WOW is a sell…any management who thinks rebranding to Woolworths is a genius idea probably is not in the business of good management…

Indulge me for a moment on that big goodwill write-down. It follows a review of business forecasts for the NZ segment for the next three years. Hunting for all that goodwill? I don’t know — that seems like kind of a lot? But also — I am not an accountant! In NZ and Australia goodwill is subject to complex impairment tests, which is very contentious. But gosh — $1.6bn? Any accountants — feel free to write in with your views.

NZL - noting continues to tick up. The Aussie deal with Roc suggests good things to come. We like NZL + ALF as a pair trade as ALF owns the mgmt contract.

EBOS - continues to be sitting “down and dirty” at $36.00 or 25x earnings. We like the quality of the company and the management — we do think it’s starting to suffer from what happens when all serial acquirers do when they get big — they need to find whales (or at least, big fish) rather than smaller firms.

ATM - Trading up, with a lot of support from the “big boys”. If you got in at something like $12.00 (we all make mistakes — ask me about Doc Martens) it’s not a bad time to slowly get out…

DGL — sitting pretty at 0.92 cents on the ASX. It’s nice to see some recovery in the price and we are hoping CEO Simon delivers us a good result come August. Noting they increased their debt facilities to $239mn, which gives them “dry powder” for further acquisitions… as and when they occur. We note Bell Potter just upgraded the stock….continue to be buy rated…think it is worth about $1.50…

Netflix had a good result; the trads have 99 problems but content ain’t one

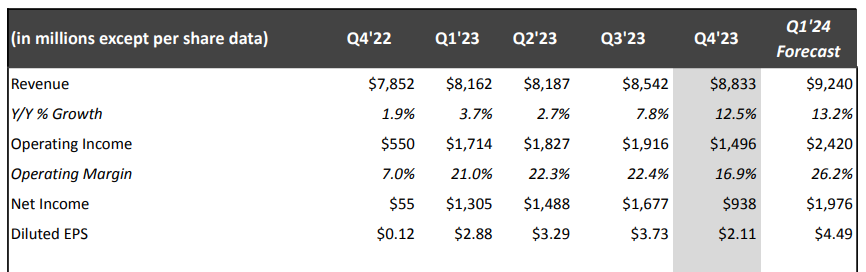

Just take a look at these numbers —

I bet Bill Ackman is sad he bought and then sold-out! Those are good numbers — a strong operating margin and strong growth — what a turn around. You know you are in a good spot when Disney is licensing shows to you.

A few things to note. First of all, Netflix went on an incredibly expensive and debt-fueled run for a number of years. To make content; to license it and to get things like The Irishman made for “prestige” even though nobody watched it. For a while this strategy was touch-and-go — subs dropped, and Disney+ had a lot of subscribers, and so did Hulu, and so on. They still do, but their streaming divisions are not profitable — unlike Netflix.

Now, to quote Michael Scott, how the turn tables — Netflix spending on content is largely flat for FY24, with about ~$17bn estimated, steady with what it spent in FY23. Disney’s is estimated to be ~$25bn for the same period. Holy Mickey Mouse!

The “trad” competitors — WarnerBrothersDiscovery, Paramount, Disney, etc, are now all stuck behind Netflix playing catch-up. They all knew they were playing catch-up, but perhaps they didn’t realise how much. Their shareholders are pressuring them to make money — hence the licensing of shows — and linear TV is a melting iceberg.

Every one of the trad competitors has got its own unique and special set of issues. WBD is loaded with debt, which Zaz has cut down but there remains a lot of it (still). WBD is also probably looking to combine with another player; the likely possibility is with Comcast’s NBCUniversal (makes sense, and is what big shareholders in WBD like John Malone have indicated they wanted from day dot — WBD was just a hop, skip and jump from becoming, uh, WBDNBCU??). Paramount is fielding interest from both Zaz at WBD and David Ellison’s Skydance. I’ve written before about the complexities of the Skydance deal — they’d likely acquire National Amusements, the Redstone company that controls the bulk of the voting stock of Paramount. That comes with a lot of debt. But Ellison’s daddy dearest is Larry Ellison, who is worth ~$142bn or so. So perhaps big daddy comes in and “helps out” with guaranteeing National Amusement’s debt. And then there’s Disney, which has had a string of bombs and is fending off attacks from Nelson Peltz and Ike Pearlmutter. In other words, the rest of the big media companies are in quite a state.

They are all trading cheap for a reason. They got problems! But they also have very valuable IP and content. Paramount has the smash-hit Yellowstone universe, for instance, while Disney has, well, Disney. We take the view that the underlying content and IP is worth more than the value of what the market ascribes to it — and we think ultimately there will be the “great consolidation” where the players become just two or three, and ultimately cable-becomes-the-new-streaming-and-is-more-expensive. But getting there — and catalysing that value — is going to be messy. And take time.

Our betting slip —

Ellison acquires Paramount, but has to buy the whole studio — Buffett and Mario Gambelli are the largest common equity holders and do you really want to irritate the single most important investor in the world? Daddy Larry backstops the loan covenants and keeps it kosher.

WBD eventually combines with a spin-out from Comcast’s NBCUniversal. Zaz doesn’t stay as CEO. Hollywood hates him.

Disney either gets an Iger turnaround or shows real improvement on the streaming side. We don’t see an acquisition on the cards.

Amazon — ??? I mean, Amazon Prime is now streaming live sports - the NFL - and it’s been a massive hit (Netflix has signed WWE to stream live). It’s a mystery to us, and it’s such a small part of Amazon’s business that we have no idea.

Netflix continues to acquire content from other studios (Zaz needs $$$) and stream live sports. As we have seen in NZ, the streaming of live sports is a big drawing card and we think it is where the entire industry is headed — streaming becomes linear becomes cable, etc etc.

US earnings tonight (Tonight's the Night)

Heavy hitters — Alphabet, Diageo, Microsoft, Starbucks

Expecting in-line results from Alphabet as they continue to suck-up ad spend — we’re interested in cloud growth there, while we predict “AI” will be said about 100 times. Diageo has been our problem child (our model portfolios hold positions in it, as do I personally) — last quarter they had logistics issues, and we haven’t seen strong results from the alcohol divisions of other ‘premium’ spirit makers — that was one weakness from the mighty LVMH. While we think the global appetite for spirits will continue in the long-run, we are not expecting anything spectacular yet. Diageo trades at 17x earnings — we like it as a long-term value play and wonder if a lot of the pessimism is priced in.

Microsoft we expect to underperform…all that AI investment and what to show for it yet? But then again, as we’ve all learned this year, if you say “AI”, stock goes up…I am probably wrong here, because AI, AI, AI — it’s the magic word.

Starbucks is another one we expect to perform quite well. We were encouraged by growth in same-store sales in China the previous quarter while the US market remains strong. China had previously been a bugbear for the co — fingers crossed China’s appetite for gingerbread lattes has come roaring back…quality co trading at 26x earnings…

I read your analysis of Netflix and the rest of the film and sport streaming services. From a local view, how does Sky TV fit in to the takeover jig saw pattern?