It's a hard time to be an art dealer selling $100 million dollar paintings

Plus: three stocks we think actually don't look awful

It’s a hard time to be a Rothko

FT - Global Art Market Shrinks as Big Ticket Sales Stall - link

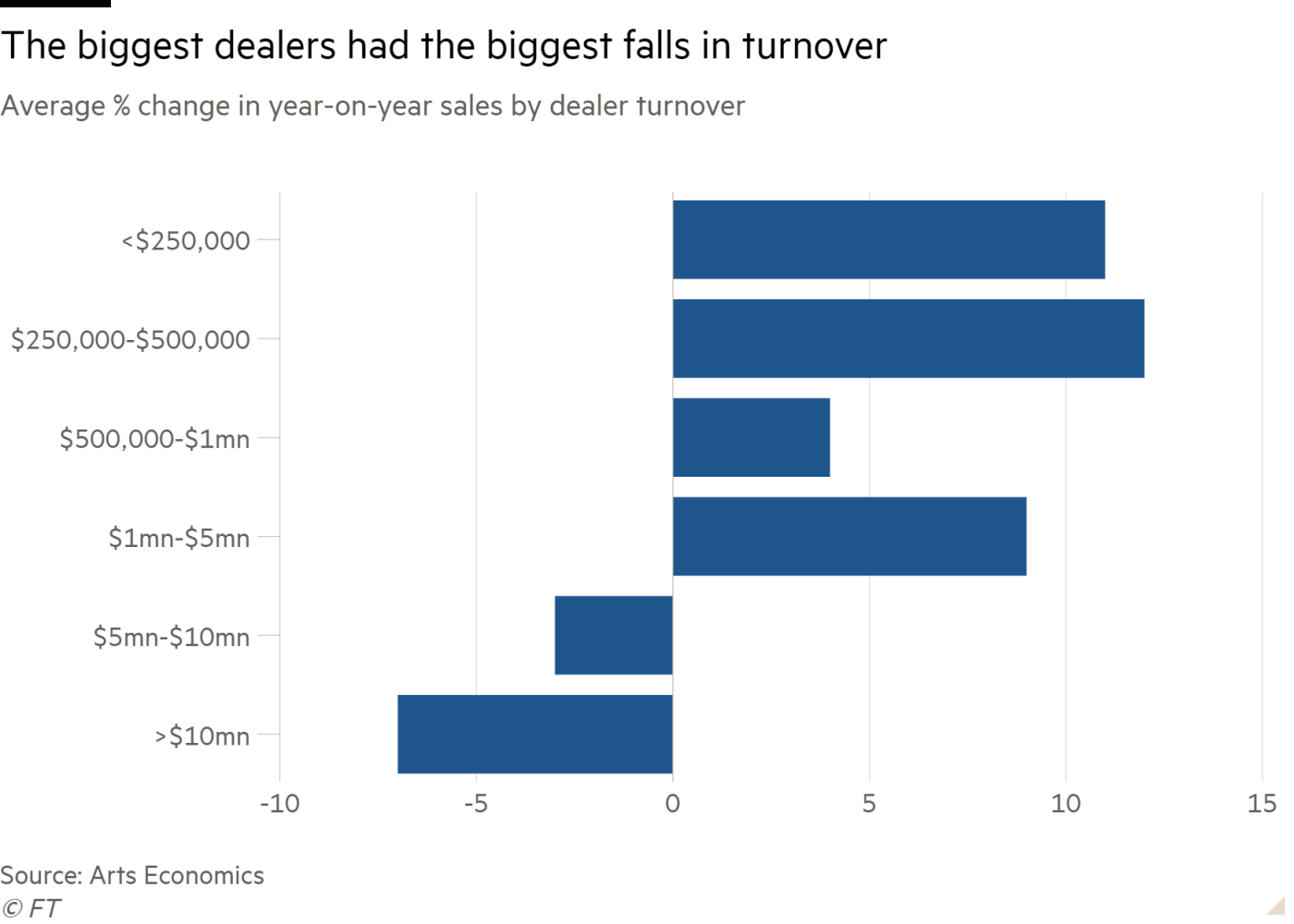

You might say it’s all doom and gloom — my last email provoked a few reactions (its reassuring my reader base agrees with me — keep writing in — I have an ego the size of Texas), though I feel like the bitcoin bros have got a laser aimed at my head (bitcoin, in my view, should be more embarrassing than it is — you shouldn’t want to admit you own something so embarrassing and tacky). Here’s more evidence of spending cooling — the global art market fell 3% in 2023 to around $65bn, while the big gallerist-dealers were reporting a 7% drop in sales. In particular that high-value market (i.e for a Rothko or whatever) fell sharply, dropping +7%

Of course this is a sign of economic cooling — when the whales stop spending (and start selling stock — looking at you, Jamie Dimon) then it’s time to take notice. The big boys always know more than you. There’s a story about Druckenmiller going short in August of ‘87 and then going long by October — he believed that the ‘market’ had found support at 2,200. He walked over to the office of Soros and Soros showed him a series of charts by a then-unknown Paul Tudor Jones. Back then Druck was working for Jack Dreyfus and went home realising he’d made a huge mistake — a crash was imminent. He called Jack Dreyfus, who by then was well out of the game — “I made a mistake” said Druck. “We need to go short. Sell it all”.

“Don’t worry”, said Dreyfus. “I sold everything a week ago. A few friends at the golf club were worried about the market…”

Old dogs know the market cycle well. Dreyfus, in spite of being an old man who mostly played golf at that point, still had a sense about things. And obviously, on 19 October Black Monday occurred and the Dow dropped 22% in a day. People don’t change, markets don’t change. Bitcoin is just another version of tulips dressed up with some fancy tech slang. No thank you.

So — the art market is cooling — and I hate to say this, but this is also what happens when you place sanctions on your richest and most loyal customers (i.e. rich Russians). They’re not going to have money to spend on a new Rothko! Poor stupid them, per Harry Enfield.

Note the AKL property market, too. High-end properties are sitting on the market for much longer — I’m not talking a little $3mn villa in Ponsonby so you can walk to Prego and get pleasantly sozzled, or sit outside SPQR with an enormous amount of work done on your face and gaze out from under your Loewe sunglasses at the poor huddled masses. I mean the $10mn + houses — they’re not selling like they used to! I don’t think National’s interest deductibility is going to do much there either — those $10mn buyers generally have cash (or a very understanding bank) and generally intend to occupy the place.

It’s a stalemate. There’s still a lot of money on the sidelines.

But it’s not all bad news…

We’re constantly running screens of our investable universe. There’s a few things that still feel like good buying — i.e URNM (uranium) on the ASX has pulled back to levels that resemble the end of last year — this is irrational given that the States is toying with banning Russian uranium and there remains a supply/demand imbalance…get in while you can. Perma-favourites like Duratec also are sold down and have erased most of their YTD gains. Note a nice comeback today from DGL — up +9.00%.

There’s also a few others we don’t think look like “bad” value (this is not financial advice, obviously it is general in nature, these are ideas we have been toying with, blah blah…) — shall we start with the most obvious and work down? OK.

GOOG — Alphabet

Trades at 25x earnings versus 34x for MSFT and whatever stupid number Nvidia is trading at now. Retains a high ROIC. Everyone has written-off Google because they don’t understand that Google has been making their own chips for a while now — i.e. less dependence on NVDA. The other thing that isn’t understood is the lack of importance of first-mover “advantage”. ChatGPT is currently the first mover in the large language model space. None of its data is its own — in theory, anyone could build a ChatGPT clone with enough dosh and computing power. Google has Gemini, which it is starting to roll out — they have $110bn cash on hand — I wouldn’t be so quick to dismiss a motivated competitor who is loaded up with cash and has its existence threatened. The question is whether GOOG can cut down its layers and layers of bureaucracy (note: MSFT has this too). This is the only tech stock that feels like “fair” value of the big 7…the rest…yeah, nah.

ERF — Eurofins

Serial acquirer of lab testing services. Did well over COVID. Stock has fallen back a lot since then to 2017 levels. It ticks a lot of our boxes — owned by a family (Gilles Martin and co — Gilles remains CEO); a CAGR of 27% over 27 years (this rivals that of Amazon, Apple and Monster Energy), a strong acquisition-focused strategy on niches that are only going to grow in importance (I’m v sorry to break it to you — but COVID wasn’t the only thing that needed lab testing; Eurofins also do the very glamorous work of soil testing and more too — stay awake, those in the back!). It’s finally sitting at a level where we’re thinking — hmm, worth it? Obviously COVID was a major tailwind but the co keeps on going — as a mentor used to say, “you make all your money in the buying…”

I mean, don’t take my word for it — read the following from their ‘23 annual report — it should be music to one’s ears:

What I love are phrases like reduce dependencies on landlords and increase the ratio of revenue per m2 by 34%. It gives me butterflies, frankly. I get all giddy like a little schoolgirl before her first prom. Tell it to me again, Dr. Martin — increase the ratio of revenue…! That’s what we like to hear — take me to prom, Dr. Martin.

I have been watching this one for a long time. Maybe tonight’s the night.

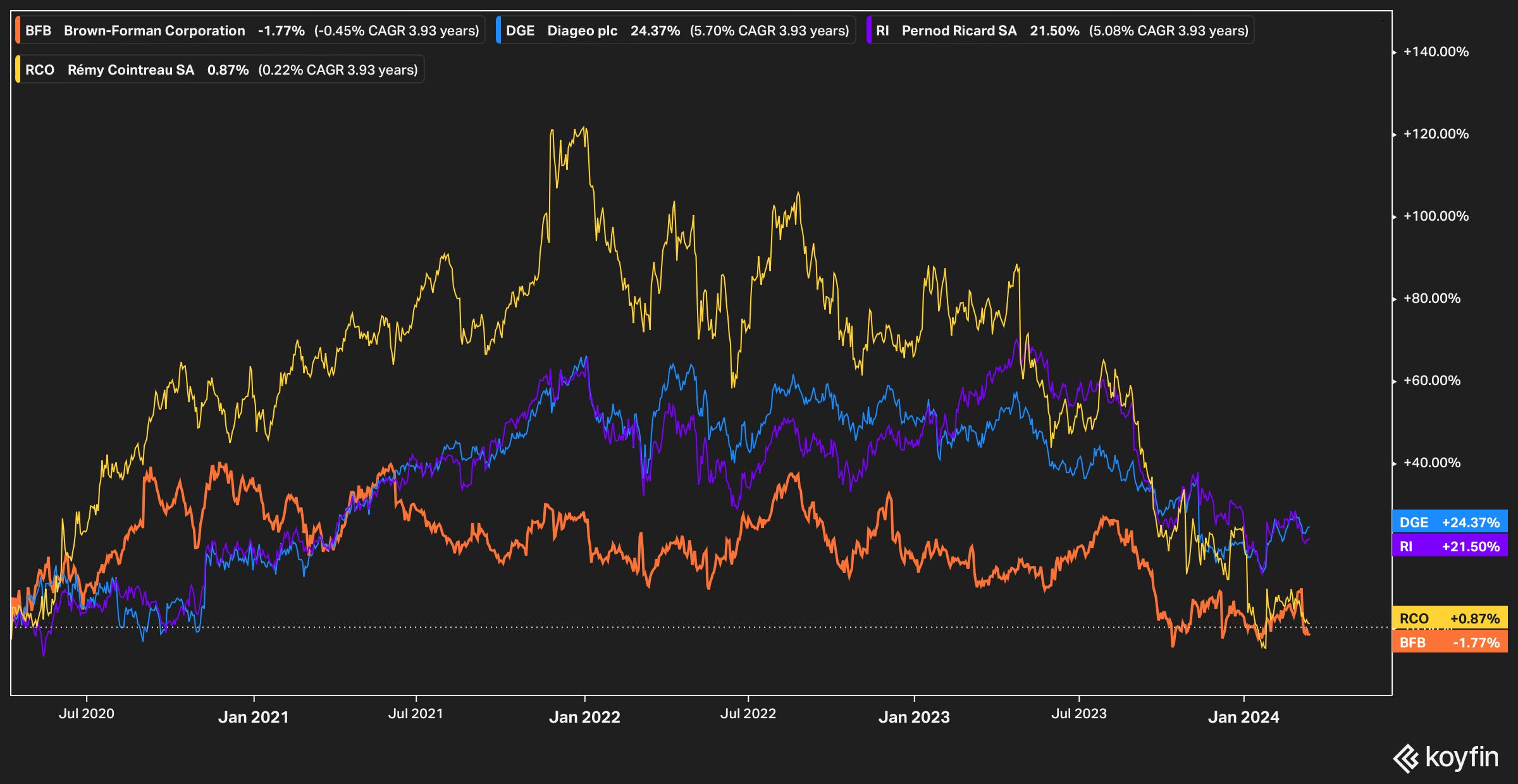

Boozers, Brawlers and Bawlers: Diageo, Brown-Forman, Pernod-Ricard and Remy Cointreau (AKA “The Bad Boozy Four”)

Look at this graph!

I mean — for a while Brown-Forman (they make Jack Daniel’s) and the two Frenchies in the pack traded at a sustained premium. They all own outstanding portfolios of booze (ironic for someone on a clean kick — but hey, I’ve been known to like a scotch or two — make it peaty, bartender). Diageo owns Johnny Walker and Guinness, and the others are more or less self explanatory (Pernod has Mumm and Chivas — cheers). They all have very good products. Believe you me — I have personally sampled them all at some point (the sacrifices I make for my readership!)

Partially the sell-off is due to inventory — Tequila (BF.B and DGE own a lot of that) had a boom time and then it plateaued a little; ditto for gin before Tequila. Retailers overstocked, and the result was slower sales. Partially it’s due to super-premium selling less (see: the high-end art market). Yet there’s still a big question mark — it’s St Patrick’s day this weekend, and I guarantee you the floors of Soul Bar will be replete with spilt booze and there will be Guinness-addled green-clad people pouring out of Leo Malloy’s joint. Could it be that these are sold off? Diageo had a rough year and it trades in London (nobody likes London anymore). The two Frenchies aren’t LVMH and are fairly small, so they too suffer from the “Euro” discount. But Brown-Forman? It’s an ‘Merican as you can get. What’s going on? This is a work in progress, and we have our best analyst (Lachlan) on it — to go back to Druck, my question is — what made it go down and what will make it go back up again.

In brief

You could just buy Mainfreight, EBOS and Infratil in NZ and forget about this whole stock thing. I’m just afflicted with a particular sickness called “value investing” — glutton for it.