An American I am quite close to asked for Manuka honey when I was going to visit her, and I forgot — of course — my mind is constantly thinking of free cash flow yields. Anyway, I went to the supermarket today to purchase some Manuka honey. I rarely go to the supermarket. With the exception of Farro and certain owner-operator supermarkets where the operator gives a damn, most NZ supermarkets are a sad indictment on the Aussie duopoly extracting ever-higher prices from us and a government that has been too scared to ever put in price controls — the former Labour government was too scared to do it last year, setting their hopes on the Grocery Industry Competition Bill, which became an act last year. I only ever dabbled in law but the piece of legislation strikes me as a piece of vague puffery with a lot of words like “good faith” and “wholesale agreement”; we all know the supermarkets don’t act in good faith and we all know they do not pass changes in wholesale pricing onto consumers — I was talking to an unnamed farmer down south who is a major supplier to the supermarkets and he said as much. Anyway, like I was saying, I barely go to the supermarket because I have a duty to support the restaurants of Auckland — it’s practically my civic duty to each oysters at Soul Bar or Gilt while the great and good of the city walk by.

Like I was saying, I went to the supermarket — now, take a look at the cost of this honey! It's practically a Birkin.

I mean, I knew inflation was bad but — gosh! And then there’s Comvita, which is the main subject of today's letter.

Selling for a relatively reasonable $43.69 (the cost of some pasta at Bossi). Comvita had a terrible week and an even worse month, selling off ~25%. I’ve never taken a lot of interest in honey and my American friend talked about Manuka like it was manna from heaven, so I thought, hold on — why is Comvita doing so badly? The world is obsessed with Manuka honey, seemingly. It’s the closest thing to a locality-guarded brand that NZ has got; i.e Champagne, etc.

Weak guidance from management prior to results — looking more like FY25 EBITDA will sit in the low 40mn range (we’re pegging around 44mn, because we think there’s a good growth story in Asia ex-China.

But it’s all China, really, isn’t it? The big thing is China revenue for the HY being down 19% on pcp. But break it down further — quarterly — and there’s some hope in China after all:

China market Q1 FY24 revenue was -26% vs pcp and Q2 revenue -15% vs pcp. Q2 FY24 lifted by 76% vs Q1 FY24, an improvement beyond usual seasonality of c50-60% quarter on quarter

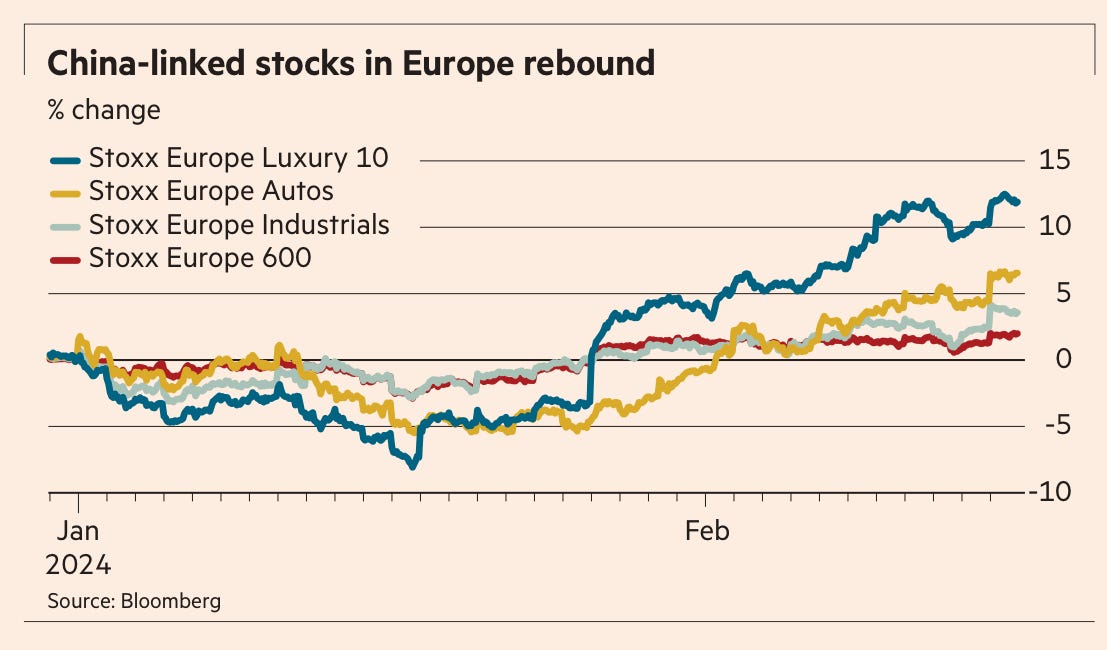

+16% is a pretty good improvement on the usual seasonality of Nov/Dec sales. We’ve seen similar bounce-back in European luxury stocks (our favourite sector) — Cartier owner Richemont reported a +25% increase in China and Hong-Kong for their most recent quarter, whereas Hermes reported similarly strong results. In other words, is China back?!

A2’s results this week will give us more colour on this — we find it hard to own Chinese equities…geopolitical risk is just too great…but there certainly seems to be an uptick in spending in the Asian luxury sector — and that’s what we like to see.

Currently sitting around ten year lows, but then again — the stock hasn’t gone anywhere in a long time. Is it good buying? I hesitate when this is how they spell “executive” on their investor relations page.

Where I’m skeptical is the North American segment. Americans are brutal — New Zealanders often miss this — we’re so “nice”! Americans, especially the business orientated ones, are utterly cut-throat — Comvita lost a big customer — sales down 37% pcp, and I’m not convinced they’ve established the brand there as premium — look at the two honey options above — they both look the same. Costco can just go ahead and cut you and find a supplier that’s cheaper. Does Comvita know how to deal with Americans? This is a serious question — you can see the success of Rocketlab and Mainfreight because they can deal with the Yanks. Looks cheap at these levels but always wary of buying a falling knife…will know more come earnings call Feb 21.

NZ preference list remains MFT RAK NZX THL EBO. Also like ARV — trading at almost half of NTA.

Fletchers & the ASX & The NZX

CEO stepped down and Chairman to step down later in the year — we called it presciently the day before. We don’t feel any glee in being right — structurally the business is a bit of a disaster and needs to be broken up. It’s been a “difficult” stock ever since the old days of Fletcher Challenge. Obviously there was money to be made buying the bottom, but structurally there are issues here which need to be looked at…rip it up and start again.

We’re watching the results of NZX limited closely this week — the ASX reported very soft results which reflect its failed project to replace CHESS — costs increased ~30%. A total word salad from ASX CEO Helen Lofthouse

We have had to manage an elevated level of expenditure given the heightened regulatory demands and the velocity of technology change and delivery in the past year – but we are highly conscious that the current level of total expenses growth is not sustainable…

Well, yeah. Tell us something we don’t know.

Zucker buys Squid Games

RedBird IMI has agreed to acquire the London-based production company All3Media for £1.15 billion from its joint owners, Warner Bros. Discovery and Liberty Media — this comes hot on the heels of RedBird buying The Telegraph and The Spectator — subject to approval. WBD is of course Zaz and Liberty Media is John Malone, who owns a big chunk of WBD too. Good deal for those two — they doubled their initially investment more or less. All3Media is behind shows like Fleabag and Squid Games. Private Equity is the obvious home for media companies at the moment — build it up, flick it on, wait for the “great consolidation”, etc. Meanwhile our friend Shari at Parmount has been having conversations with Brian Roberts at Comcast — I love how much she’s making it obvious the company is for sale. My bet is still on David Ellison buying it (another RedBird backed venture) because Roberts has always wanted to marry WBD. I should also make mention that Buffett has recently sold 1/3rd of his stake in the co. Et tu, Warren? Or just offsetting gains made from trimming part of BRK’s stake in Apple?

The whole blood facial thing

I talked a while ago about Puig acquiring a majority stake in Barbara Strum — it’s skincare you can buy at Mecca for the cost of a nice bottle of single grower champagne. Here’s the numbers — $240mn for 60% of the company with the rest of the company to acquired at a later date. Puig also owns Byredo and Charlotte Tilbury — they've made some of the smartest bets in beauty, versus Estée Lauder’s disastrous run. Strum has murky credentials but is a marketing genius — she famously took the blood of her client’s and then would mix it into her facial cream (clients include GPow, Kim K, Oprah…)…there’s a lot of speculation that Puig will IPO later this year…we are watching closely.

Briefly noted — A Broker’s 34-Year Wait for a Stock-Market Boom

Inside Johnny Depp’s Epic Bromance With Saudi Crown Prince MBS

The country’s most secretive billionaires are about to get much richer