Paramount finally sold | Is Deciem enough to save Estée Lauder?

Last media baron standing

It’s been seemingly forever but Shari has agreed to sell Paramount? As most thought, Shari is selling to Larry’s son, David (Ellison) — David will buy Skydance, the family holding company, for $2bn, and he’ll buy out 50% of Class B Paramount shares for about $15 per share (class B are the peasant class shares — the ones with practically no voting rights that ordinary Joe Bloggs like Buffett and co own).

It’s not much of a surprise — a sale to Apollo/Sony would’ve meant scrapping the whole thing for parts. This deal means Ellison (and RedBird, his partner in the transaction) will own 2/3rds of Paramount and class B shareholders owning the rest of the “new” Paramount.

But where does that place Shari? Just another billionaire now — without the apparatus that once was almost as powerful as newly-married Rupert Murdoch (mazel!). It’s also a kind of gravestone on the twilight of the media barons — there’s a couple of families still in control (Murdoch for one, sans the 21st Century Fox assets; also Rogers Communications in Canada, Roberts at Comcast, etc). Paramount is a masterclass in ego and mismanagement, though — it came into the streaming era kicking and screaming and never quite took off; but even before then, while Sumner (Shari’s daddy) turned the company (then Viacom/CBS) into a vanity project built to fuel his ego while Philippe Dauman mismanaged the business (well worth reading this NYTimes article about the downfall of Dauman).

As for Ellison — he has an uphill battle to make Skydance/Paramount work. Skydance has had a few hits — Top Gun, Terminator, but it now has inherited a motley crew of media assets and an empire in disarray. Lots of house to clean and lots of competitors on the sidelines, all of whom are having similar issues in their own way. Good luck, David.

Last Deciem attempt

I've written a lot about Estée Lauder — early on in my “investing career” it was one of my favourites, and rightfully so — the company got so much right about the YouTube era of beauty vloggers — they had the best parties, the best “influencer” retreats, their PR at the time was on-point (shame it isn’t now??). And the YouTube beauty gurus got older, of course — they got married and divorced and married again and had children and the girlish, pure, youthful fascination with trying out products, doing “hauls” and interacting with their audience was replaced by “life”. And EL, bless their hearts, never quite regained the magic — it rode a spectacular wave before overstocked inventories, changing consumer tastes, a slow-down in China and competition from other brands put the stock on a one-way train to slumptown.

The rise and fall of Estée Lauder

EL’s biggest misses were brands they did well off during the glorious YouTube era — Smashboxx, Too Faced, etc — they had to write down the value of both those brands because, it turns out, what the YouTube era loves the 2020s era doesn’t give a damn about. But throughout it all EL had their majority holding in Deciem, the owner of The Ordinary group of products. The Ordinary is still a great brand — active ingredients for cheap! — that success has been reflected in EL’s sales, which have bolstered every (disappointing) quarter. Now the co has completed its buyout of Decimen — it paid in total $1.7bn for the whole lot. It’s a much better deal than what the co paid for Too Faced ($1.45bn!!), considering Too Faced has been eclipsed by other beauty brands — especially among the all-important tween/teen market.

It’s smart of finally buy the rest of Deciem — its been a saviour to EL for the last few quarters. But is it enough to turn around the fortunes of the company? Now, let’s not act like the thing is going bankrupt — they earn plenty — but look at the competition: there are the two big Korean beauty groups, LG H&H and Amorepacific, which manufacture the bulk of what you will find at Hikoco, my favourite store (if you want cool fresh energy, go there). Korean skincare is just excellent and cheap — I could not live without my Isntree sunscreen. There’s also the smart acquisitions that companies like Shiseido have made (Drunk Elephant) or the recently public Puig’s portfolio of brands (Charlotte Tilbury, etc). Competition has increased and the train has moved on…YouTube vloggers who?!

Fabrizio Freda, CEO, allegedly doesn’t want to let go of the reigns (he was responsible for that giant rally, to be fair). But I’m not sure if he is the man for the job — EL has a lot of legacy brands in need of rejuvenation and its Hail Mary of selling through Amazon (I’m not kidding) excites me about as much as watching grass in Gore grow. In the meantime, its Korean and European rivals will continue to gain ground (that includes L’Oreal, btw, which has managed to navigate the currently environment impressively).

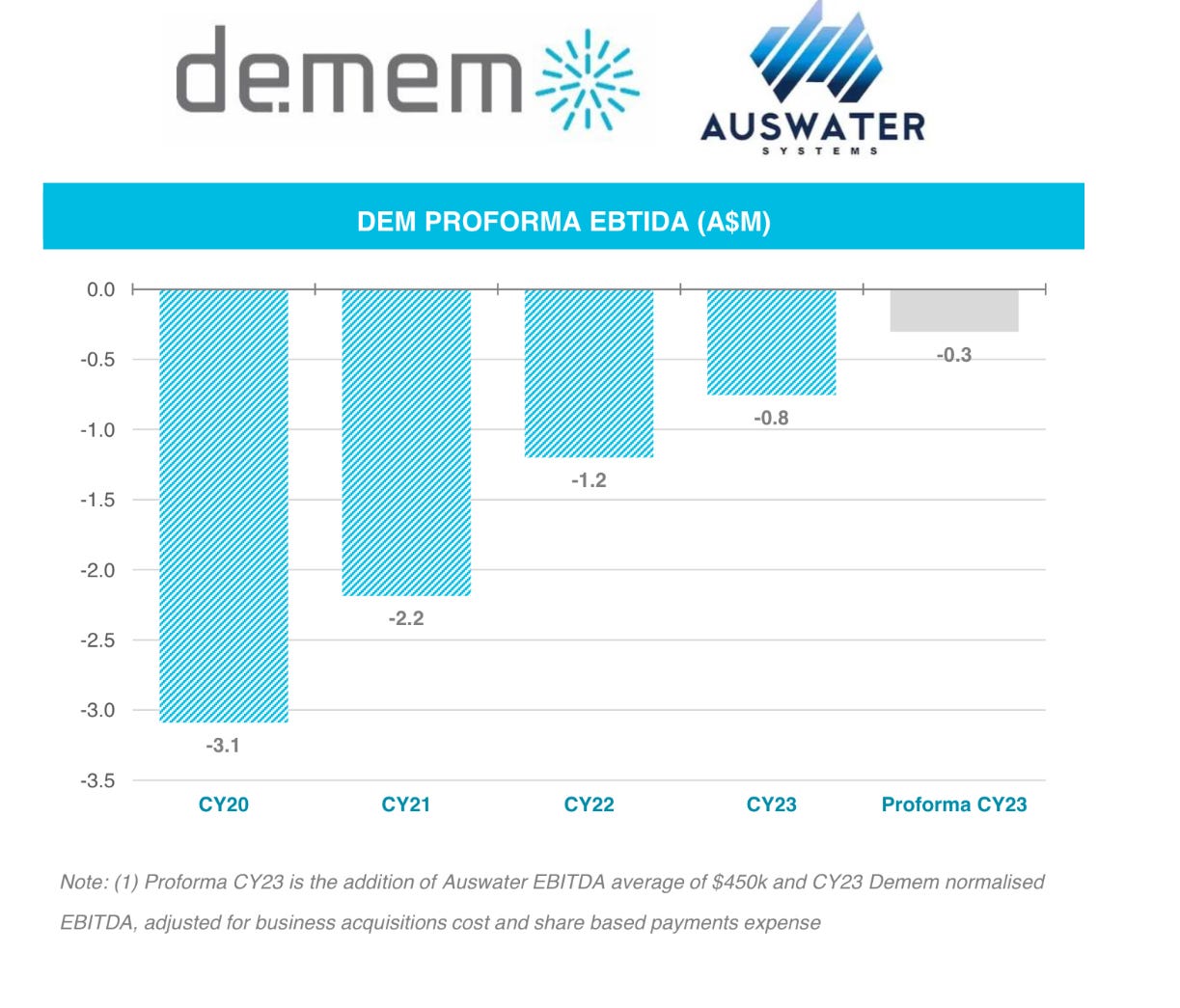

H2go — De.mem’s new acquisition

We refreshed our coverage on water treatment De.mem last week — y’day (was a public holiday here — happy b’day Charlie) the company announced the acquisition of Auswater — a Perth based water treatment company. Paying 4x EBITDA or 1.3x revenue… reminds me of the strategy undertaken by Pool Corp over in the US where it buys regional players until it has de-facto controlling market share. The acquisition brings the co to near-EBITDA breakeven — I imagine this is accretive to future bolt-on acquisitions. Note the chart below…

We continue to like De.mem — I spoke to management last week and continue to be impressed by owner buy-in and the long-term mentality. Given potential of i) its graphene filter technology in overseas markets and ii) a continued strategy of rational bolt-ons it feels like a good long-term stock to hold… see cashflow-positive by FY25…

NZ

Synlait — Kaput. Can Bright Dairy please take it private already? You want bonds with that? Says it all…

RAK — As I wrote last week, don’t see any rationale for the stock trading so low. If deal doesn’t go through is at least a $1.00 stock (based on our blended peer comps) if deal does go through it is +100% upside. Happy to hold this thing either way. NBIO still is in the works, so…

EBOS — Continues to exit the MSCI index (don’t think there was enough volume to exit fully on Fri, per my back of envelope math…suspect exit may have happened today?). New CEO in the co’s MedTech space suggests where the co sees value… given the depression of the share price after it left MSCI index (so long, thanks for all the fish) we still like it as a buy…

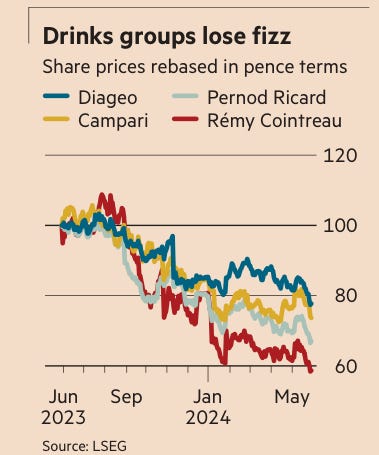

Chart of interest … Booze barons

Love this image — we hold both Pernod Ricard and Brown-Forman (not on the chart!) in our wholesale fund, The Rough Point Fund. The liquor makers have been trading down and dirty and are trading at 10+ year lows. Love a bargain…