Rate cuts for everyone

Why 50 bps is nice but the RBNZ's reliance on the housing economy is a worry

I was out the other night, and a blonde lady, upon finding I out do “finance”, breathlessly said to me “aren’t you delighted at the 50 bps rate cut?”. I didn’t want to be rude and tell her what I really thought (she worked in property, and as we all know, the property crew in NZ are beyond delighted with the rate cut, because the formula for large capital gains in property in NZ is largely based on low interest rates). Of course, I am not opposed to the rate cut at all — the RBNZ behaved as if it were the bank of a large country rather than a small entity such as NZ (i.e. Orr, for all his arrogance, would’ve had the right idea had he been dealing with an economy like the EU, UK or USA. But he wasn’t, and isn’t). The rate cut is a nice thing from psychological point of view — but in practice, a lot of people are already on mortgages at a higher rate, or paying debt at a higher rate, etc. It is not a magic wand that makes everything better.

The tools of central banking are exceptionally crude. You can make rates higher or lower or print money. There’s variations on that, and economists will protest and say it’s “much” more complicated, but they would, wouldn’t they? The point is — we have an economy in slowdown, where spending is constrained and the average salary worker has experienced significant lifestyle changes — mostly to the downside. Which is why I found this statement from the RBNZ so interesting — housing is a major concern of Orr’s, it seems:

More generally, weak house price growth, lower levels of net immigration, and ongoing fiscal consolidation from spending restraint, are expected to constrain aggregate demand growth

You don’t need to be much of a genius to work out that the NZ housing bull market came from i) price growth (reflexivity) ii) high net immigration iii) no capital gains tax and iv) excess demand vs supply. That statement, led by house price growth, is telling of where the RBNZ sees NZ’s economic future: that is, house price growth lollapalloza! Let the good times roll!!!!

I find that interesting, given that our current ruling party has stated house price affordability is a key issue. Here’s housing minister Chris Bishop saying that “house prices need to drop”, backed by his boss, Chris Luxon, who says that “downward pressure” is needed on house prices. So on one hand you have Orr and the RBNZ decrying the “weak house price growth” and on the other you have our PM and his ministers saying “house prices need to drop”. You do not need to be a genius here, either, to realise that these statements — from our reserve bank and our PM — are at odds with each other. They are contradictory.

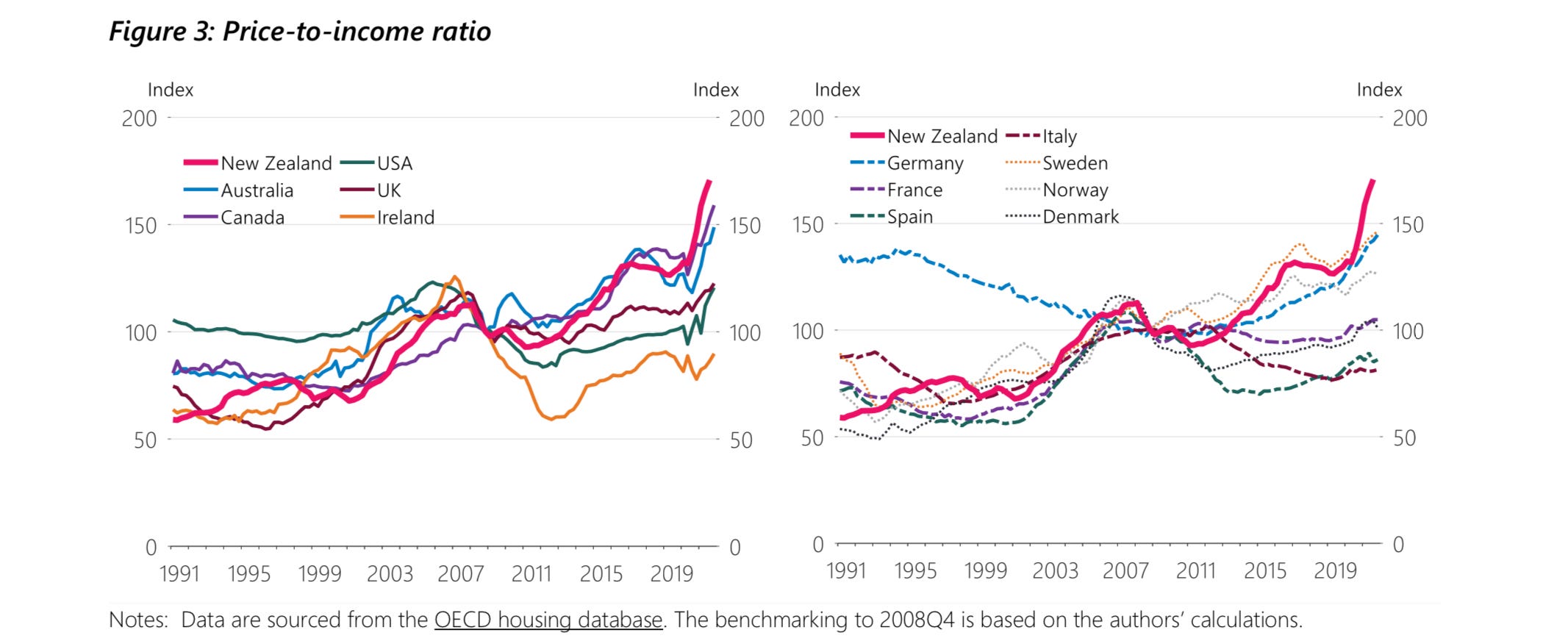

The dirty not-so-secret is that house price growth has driven the NZ economy for the last 15 years. Here’s data from a RBNZ paper, published in 2022. The price-to-income ratio for housing in NZ is the highest in the developed world. It far outstrips much larger economies, like the US, or economies with closer access to markets, like the UK and Ireland.

(There’s a small irony to all this — housing construction costs are also among the highest in the world — and yet still Fletcher Building can’t make money! Talk about being run by bad managers!)

This presents the RBNZ with a problem. If NZ’s “economic miracle” is from rapid house price growth, what does a reserve bank do when people are leaving the country faster than they come in, and there appears to be no other strong economic driver? Well — the simplest answer is to increase house prices more! Like I said — let’s keep the good times rolling!

This is a bad approach, though. It’s bad because it is predicated on ever-increasing levels of capital to buy and finance said housing. But if people aren’t making capital, because people aren’t spending, then there’s not much capital to go around.

Look around at a restaurant the next time you go out. How busy is it? If you know liquidation and bankruptcy lawyers, ask them how busy they are. Walk down Queen Street, Ponsonby Road or whatever road is nearest to you. Note the amount of empty retail space. Note the empty shops. I have been to multiple events recently where people are afraid to say the word “recession”, like they will summon Voldemort, or the Candyman. Everyone is too afraid to face reality square on.

This is the real economy. I don’t consider the made-up fugazi gains of property to be the real economy because they’re largely paper gains (you only need to look back to 2008 — to the US and Ireland, etc). The real economy is people being paid and shopping for things they actually need or want. The real economy is money circulating around in a fashion not dissimilar to a medieval village — you shop at the supermarket, you shop at the petrol station; you get paid from your work, etc. That ‘real economy’ is facing issues.

The best way to get an economy going is to make things people want. This is why the US is so great — they have an economy with a lot of things people want. Australia does well, too, because they have an economy based on mining things out of the ground (you can be as ‘clean and green’ as you want, but you need to get stuff out of the ground from somewhere). What does NZ make, other than dairy, that people want?

An example. A long time ago NZ merino wool was considered the best in the world (it still is, in my opinion). There are old factories in the north of France which still have “NEW ZEALAND MERINO” emblazoned on them, in fading writing. The Secrétariat international de la laine used to be partially sponsored by the NZ merino industry and held the competition that discovered both Yves Saint Laurent and Karl Lagerfeld. Merino, in other words, used to be as synonymous with quality as Loro Piana is now. What happened is typical NZ (and Aussie) mishandling of IP. We fumbled the bag, we got too distracted by big numbers, we sold it to the highest bidder — whoever they were — and now merino is the sort of wool that makes thin Glassons skivvys. There are old hands down south who used to do wool grading and so on and they will tell you the sad story of how we devalued a once-premium product.

We do this all the time. You can buy NZ lamb and beef in France cheaper than you can in NZ. We’re so good at devaluing what we have. We also fumble the bag out of self-righteousness — Gabe Newell, the billionaire founder of Epic Games, wanted to relocate staff to NZ and invest in the country during COVID. The then-Prime Minister said no. It was about “fairness”, she said. I am not sure what economy cares about fairness and precious self-righteous back-patting rather than making money.

You can see where I'm going with this. It works to have extravagantly priced housing for a time — you get (theoretical) gains and the service industry around it makes money too (not to mention those who sell the mortgages). But if you don’t have an engine around that, you end up with an economy that prices people out of owning their own home. You end up punishing your own citizens, which is not a good incentive to live in the country (you only need to look at how many citizens leave to across the ditch…)

I am rarely in praise of Luxon or the government, but they’re right here — house prices need downward pressure. A well run economy should be able to offer its denizens housing, time off, recreation and activities that fed the mind and soul as well as provide pleasure. In other words — panem et circenses — bread and circuses! (The ancient Romans knew what the people wanted).

This is what I thought when I bumped into that blonde girl who breathlessly asked if I was pumped about the 50 bps rate cut. Sure — it’s a good thing. But there’s so much work to be done — I think the biggest thing is changing our mindset (I’ve written this before). We’ve unfortunately had schools where teachers focus on churning out rule obeyers when we need more rule breakers.

I will finish with something cheesy. Take it away, Steve —