Fletcher Building, Lina Khan Game theory and more

At the end of the day, there are ALWAYS club sandwiches

Report from the front — Fletcher Building

I suspect chair Babs Chapman “had” “COVID” since she’s done an abysmal job as Chair and board member. If you need qualification for that (“but she’s a highly respected director, Eden!” I hear you say) the stock price was around $6.00 when she was appointed as a director, in 2018. It’s now around $3.00.

That’s OK though — Peter Crowley did a great job as substitute chair — frankly, he’d make a great chair — he was humble and contrite and won over a very jaded audience. He admitted that calculating ROFE (return on funds employed) without including unusual items, significant items or write-offs doesn’t make sense — that was my question, so I’m happy to see future change there, hopefully. Cathy Quinn made a bizarre pitch for staying on-board — she’s “not a quitter” and “she wasn’t even paid to be on some committees” [sic]. Much like Lorraine at Rakon, I find it bizarre when board directors beg to their shareholders like sick children of Africa. These are wealthy and connected people, remember. Cathy Quinn may have had a great career elsewhere, but she’s been an abysmal Fletcher director.

One fellow stood up and said, “you know, I was here in 2018 when you [Cathy] and co were appointed, and I thought, let’s see how these professionals go — accountants and lawyers etc. Well, it’s 2024 now, and now we know. Hasn’t gone very well.”

Nevermind, though — more importantly — there was a brigade, as there always is, who lined up for the free savouries and sandwiches after. There was a line! The man serving the sandwiches and savouries implored them to use the tongs! See documentary proof, from Eden S Thompson, below:

It is comforting to know that however terribly Fletcher Building has done, it can always afford savouries and sandwiches for its long-suffering shareholders.

Fashion land

Why are they so excited?? They are EXCITE!!

Lots in fashion and beauty land today — the FTC has blocked the merger of Capri and Tapestry, in a rare win for Lina Khan. Also, Estée Lauder has a new CEO —Stéphane de La Faverie. Lauder has been embattled for seemingly forever, but really only the last couple of years as the world moved on from the maximalist ho-ha of Smashboxx and beauty YouTubers). Finally, a smattering of results — Hermes outperformed (the below meme, showing Business of Fashion’s headline before and after results is hilarious), while Kering disappointed — though the stock is up on the news, perhaps because once you’ve hit rock bottom there’s no place to go other than up.

But let’s talk about the FTC, first. Lina Khan gives off head girl energy — like she has aced all her tests at school and has a perfectly pressed blazer. She loves suing companies! She has sued almost every major American company — Google, Amazon, Meta… our girl Lina loves to sue! She’ll sue ya!

Usually her lawsuits are like: Amazon is a monopoly so it is anti-competitive. Or: Meta is a monopoly so it is anti-competitive. You get the gist (by the way — gist isn’t a word I’m told?!). They usually fail — Khan sued Microsoft from acquiring Activision-Blizzard, on the grounds that it’d give Microsoft an anti-competitive advantage (largely due to Activision owning Call of Duty). It didn’t work — Microsoft was happy to license out CoD and other games to Sony’s Playstation brand, etc.

In a sense though, all of Khan’s lawsuits are successful as they end up costing a lot to hire lawyers to defend against said lawsuits. Especially in the case of a merger. In other words, Khan extracts her ounce of flesh one way or another. I remember having lunch with Julian Miles, the wonderful KC, many years ago. He said it was a great time to be a lawyer during the GFC. We all made money! Similarly, it’s a good time to be a lawyer during the reign of Khan.

One lawsuit that did succeed is the merger between Capri and Tapestry. This is surprising given what Capri and Tapestry deal in — Capri owns Versace, Jimmy Choo and Michael Kors, while Tapestry owns Coach, Kate Spade and Stuart Weitzman.

What is the first thing that you notice about these brands? I mean — at the risk of sounding impolite, they’re not exactly top of the range brands (with the exception of Versace — a brand that should do better, but hasn’t). Coach or Kate Spade are sort of “my first handbag” kind of outfits. They’re not Hermes, or Louis Vuitton, or even Burberry. It’s kind of a merger of mediocrity with more mediocrity. This is perfectly fine — I’m not knocking it — there’s a place in the market for brands like that — but the judge’s ruling against the merger is bizarre to say the least.

It hinges upon the idea that the two companies, merged, will create some kind of stronghold on the “accessible luxury” market. But even then, the ruling and the FTC appear confused about what they’re talking about — at one point they refer to mass-market handbags (talk about defining a category so widely you could drive a truck through it).

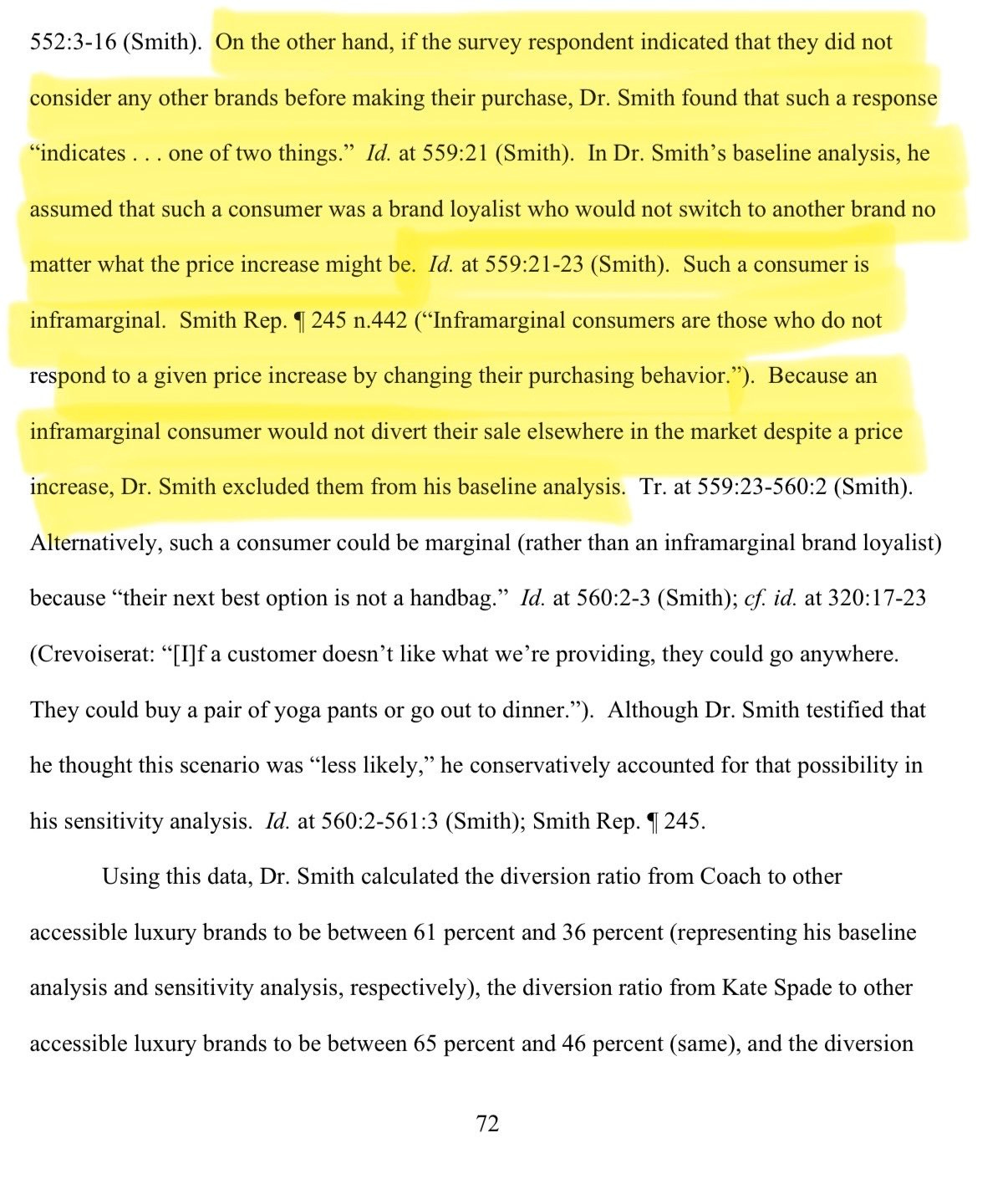

I mean — are we talking about accessible luxury or mass market here? But the ruling gets even dicier, when you consider that the study the judge leans on excludes inframarginal customers (i.e. brand loyalists). See below (it’s wordy — stay awake those at the back):

I don’t need to tell you how vexing and nuts it is to not include brand loyalists — that’s what powers companies — loyalty! But there’s a few other false equivalencies made, too — for instance, Coach bags are more expensive than Michael Kors bags, but the study the judge references infers they are comparable. They’re not, of course — they’re both mediocre, but mediocre at different price points. And price points matter!

Capri stock cratered on the ruling. Down 49%!

Here’s a very speculative play (don’t take my advice use your own brain I am just a monkey at a keyboard!): if Trump is elected then there’s a possibility the ruling is overturned. There’s also another factor at play — the fact the judgement relies so heavily on some dubious data and surveys.

The question you really want to be asking is does a merger between Capri and Tapestry affect the the price of the goods sold by Capri and Tapestry. And the answer is more like — well, maybe, if you exclude every other accessible luxury brand out there. Which feels, again, a little out of touch with reality — there’s more accessible luxury brands (and bags) than you can shake a stick at: nobody, except perhaps Lina Khan and the FTC, believes that this merger is particularly anti-competitive.

So again — the trade might be — buy some Capri and wait for the election. Not advice! Monkey at a keyboard1!! Remember??

OK TAKE A BREAK FROM FASHION STUFF NOW

How about Aussie land? G’day!

Well, DGL, a company we’ve been tracking for a long time, finally had a good month —

If you were buying around the 0.48 cent level you would’ve done well! The premise behind DGL, basically, is that it’s so cheap. At 0.48 cents it was trading around 1/3rd of book value. A correspondent wrote to me and said “it’s probably the cheapest thing on the Aussie market” (I’d be inclined to agree). So, you know, reversion to the mean — it isn’t a particularly spectacular company or stock, but it’s done nicely, thank you v much.

Also Duratec, likely my favourite company in Aus. It keeps winning contracts and laying down track. We like that. It’s also founder-owned (three dudes who piled together their money). We like that too.

‘Struth.

Oh — also, Titomic is up about 20.00%.

BACK TO FASHION LAND NOW (sorry not sorry)

Let’s talk about Estée Lauder, which has done terribly quarter after quarter.

I’ve written on the reasons for such terrible performance before, but in short: the company did very well during the 2000s/2010s — it was buoyed by the rise of YouTube “beautytubers”, and by maximalist brands like Smashboxx and Too Faced. They made a lot of acquisitions and for a time, they paid off. Until they didn’t.

Partially this is because the audience got divided — the audience who used to go to Mecca and buy, say, Smashboxx, now goes to Hikoco and buys Korean skincare. (Plenty of reason for this — the Korean products are better, and cheaper). Partially this is because Lauder overpaid for a bunch of those companies it bought back in the heady 2010s. And partially, it’s because they failed to see where things were going — make-up is marginal; skin care is everything.

Now we see a new CEO — Stéphane de La Faverie. They needed one, because while Fabrizio Freda was responsible for so much growth, he was also responsible for the dinosaur-like response Lauder has had in the 2020s (it is worth remembering that just because you were good at something a decade ago does not make you got at something in the following decade). La Faverie was responsible for Lacomme’s success at L’Oreal. The stock is sitting around $80.00 (well off the heyday of near-$400.00). I don’t, honestly, know whether it’s worth buying it or not — the bull case is basically — here’s a company that still makes c.$15bn in revenue (i.e. trading at 2x revenue).

Let's apply the same logic we took to DGL here — remembering that DGL is the classic case of “trading so low that rock bottom got a new definition”. At $80.00, Lauder could probably endure a sell-down until $60.00 — but remember, the sellers have mostly been bought out by now — a security will only go down as much as the sellers will let it — once the sellers have been washed out, then, there’s little more to do. Ditto multiples — Lauder traditionally traded around +25x earnings. Premium trades for premium. If La Faverie makes a difference, then any upside is profit for buyers. That’s — somewhat compelling?! I don’t know. I’m almost convinced. Almost.

Kering & Hermes

Tale of two halves. Hermes smashed results because everyone, including half your wives and girlfriends (do I get a Northern Club membership yet?!), want a Birkin and they can control supply and demand. Kering did not, because less people are buying Gucci. One bright spot there — Bottega, which saw a modest uptick in sales.

I’m not particularly concerned about Kering. It’s already at the bottom. They retain a lot of prime real estate and continue to still sell a lot of clothes - and bags — and jewellery. I don’t think the market is concerned either, as the stock bounced on the news. When everyone thinks you’re dead, any sign of life is a nice surprise.

The truth is — and I’m admitting it now — is that BBR is in fact written by 40 monkeys sitting in a room at typewriters, and every third page is legible. You know, the old saying, if enough monkeys sit at a typewriter they’ll write Shakespeare…