I know Cognac isn't cool or hip, but hear me out...

Plus: LVMH, Potentia and Rakon

NZ

Potentia — Here’s what’s happening at the moment with Visa, the cinema software company. The private equity firm Potentia would like to buy Vista. Nobody else appears keen on the offer. There’s also this Potentia-linked Bidco, and I'm not saying that means it’s a Bidco for Vista, but it’s not not a Bidco for Vista either.

The problem is, as I said, nobody else seems to support Potentia’s goal to Buy The Company Cheaply. Then again, everything for the right price…

Rakon — reiterating what I said the other day. Barclay, at GS, says of M&A activity he has advised on: “some of which appear likely yet to be fully played out”. Keyword is yet. More in the pipeline? It ain’t over ‘til the fat lady sings…

LVMH

Whisper it quietly — recession is here — LMVH revenue flat on 9 months, whereas Q3 saw revenue down -3%. “Cadence” there is reflective of a weaker environment — i.e. people are spending less because we are in a recession (in all but name — call it a ‘vibecession’).

Reasons to be cheerful? +3% growth in perfumes & cosmetics and slight growth in selective retailing (Sephora, DFS, etc). It’s not much, but you gotta be cheerful about something in life (my guess is that Sephora’s biggest US competitor, Ulta, is seeing a bit of a decline and Sephora is picking up the slack).

Continued weakness in wine & spirits albeit some Cognac growth in the US — obviously China continues to weigh on the Cognac market (the booze racket had a less bad quarter than it had in Q3 2023, where it saw a -14% decline).

More or less flat results in both fashion & hard luxury (watches, jewellery). There’s not much more to say about this other than people are obviously spending less as they’ve been walloped by high interest rates and an inflationary environment the last few years. Inflation looks to be cooling down, so it’s a question of where we are in the cycle. I’m not convinced we are quite out of the woods yet.

LVMH stock is trading at a -29% discount to its historical 2 year P/E (blended) and a -26% discount to historical EV/EBIT. On a peer basis it is trading -29% under our universe of stocks (20.5x P/E vs 28.9x). I am picking up more here. Are you doing the same?

What’s the Cognac read-thru? Or: the case for Cognac

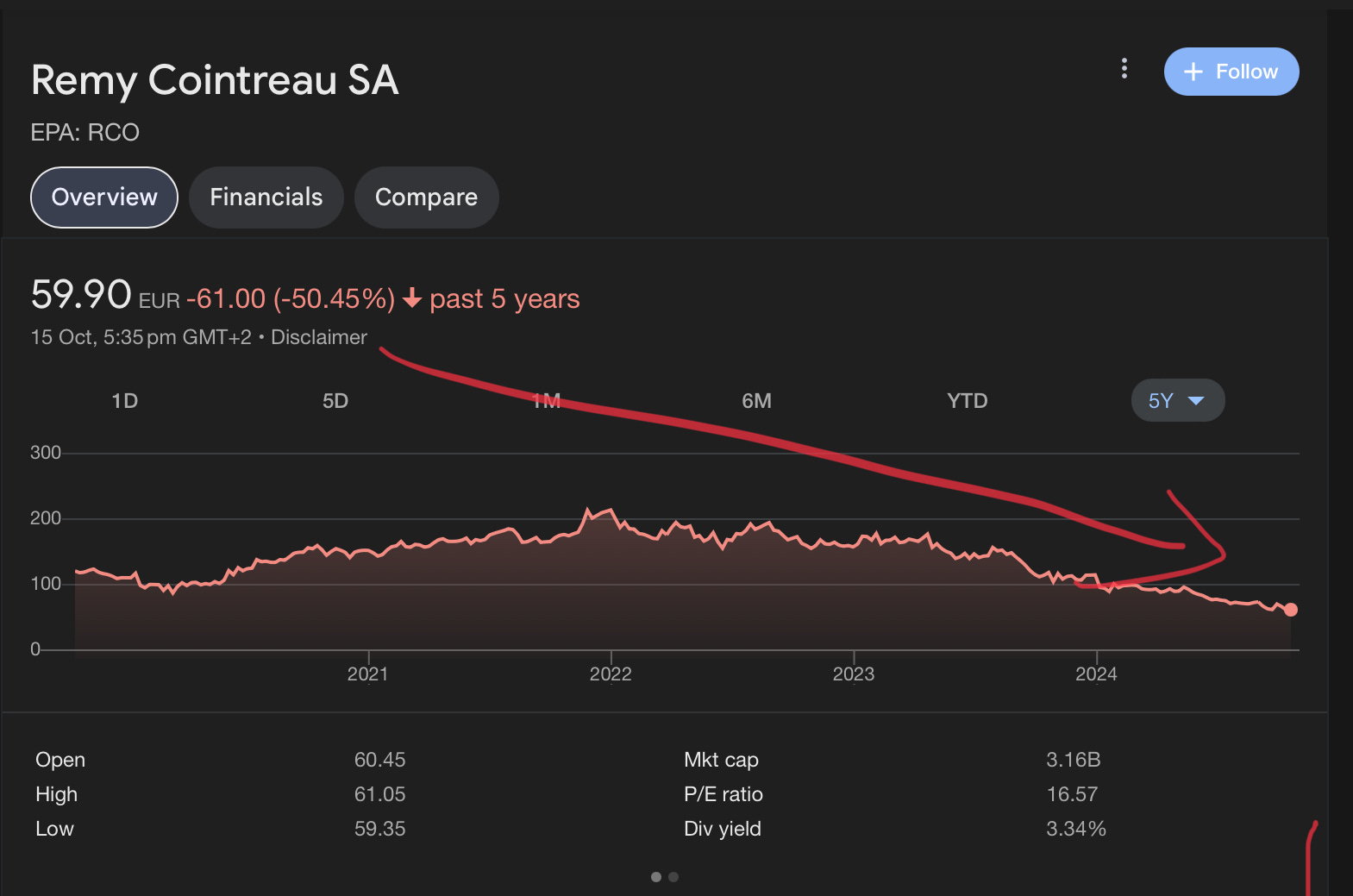

Right now you can buy Remy Cointreau for 59 euros per share. That’s more than a 50% discount to what it was trading at five years ago. Find my hard hitting TA below.

I’ve been sitting on my hands watching this for a while. Remy makes a lot of Cognac, as well as (surprise surprise) Cointreau. They also own Bruichladdich, a whisky I am particularly fond of1 . They are a 300 year old company. They’ve been hit particularly hard by the China thing.

What is “the China thing”?

China is a massive consumer of Cognac. Chinese consumers also tend to buy the most expensive Cognacs. The EU is putting a levy on China-made electric vehicles (about 45%). China has retaliated by requiring importers of brandy (and Cognac) originating in the European Union to put down a deposit on the value of the inventory of 34 - 39%. If you’re importing Cognac, particularly expensive Cognac (the ones that Chinese consumers love so much) then you’re going to find yourself in a world of trouble, because you’ve got to find almost 40% of the value of your import before it’s sold and before it even hits the port.

Of course, the Chinese government doesn’t really care about Cognac too much. It cares about hurting Europe where it really hurts, because of those EV tariffs. It’s pure lunacy, in my opinion, for the EU to impose such massive tariffs — frankly if China can produce better (& cheaper) EVs, then more power to them.

Don’t worry too much though

This is a trade spat and trade spats have a way of working themselves out. The higher-ups in China want Cognac, and the Cognac lobby is not insubstantial (remember France’s richest man, LVMH owner Arnault, has in interest in the success of Cognac too). It will no doubt affect RCO and peers in the short term, though.

Inventory that goes up in value

Here’s my favourite part of the equation. Imagine you have inventory. Maybe you sell widgets or fidget spinners. I don’t know. Usually the value of this inventory goes down because it is old, and there is less demand, and people want the new thing. This is why you see end-of-year clearances at the shops because the shop owner needs to clear out inventory. Now imagine you have inventory that merely goes up in value (what’s in there? Mona Lisas? Picassos? The Holy Grail??). Well — you’re going to be in the minority with that, one of the lucky few. What are you selling??? Where are those Mona Lisas?

Liquid assets

Cognac only gets more valuable the older it gets. RCO has been going for three centuries. Deutsche Bank estimates the value of Remy’s inventory of old stock (some of it dating back to the 1700s!) at 117-234 euros per share. That implies, for the mathematically inclined, an upside of 98 - 296% per share. In other words, I can buy a share of Remy today for 59 euro and own a proportional share of their aged stock that’s worth 117 or so euros. That’s a tempting proposition.

Price > Narrative

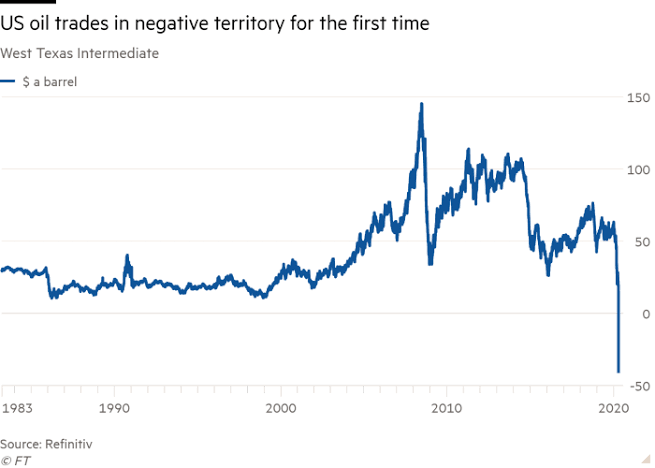

It's important to remember that price drives narrative. Do you remember when oil sat at $0.00 a barrel? Here’s a refresher on that:

Yes, it was totally normal and OK that oil — a product that is quite needed by the modern world — traded at $0.00 a barrel (and below — people were actually paying you to take oil off their hands!2)

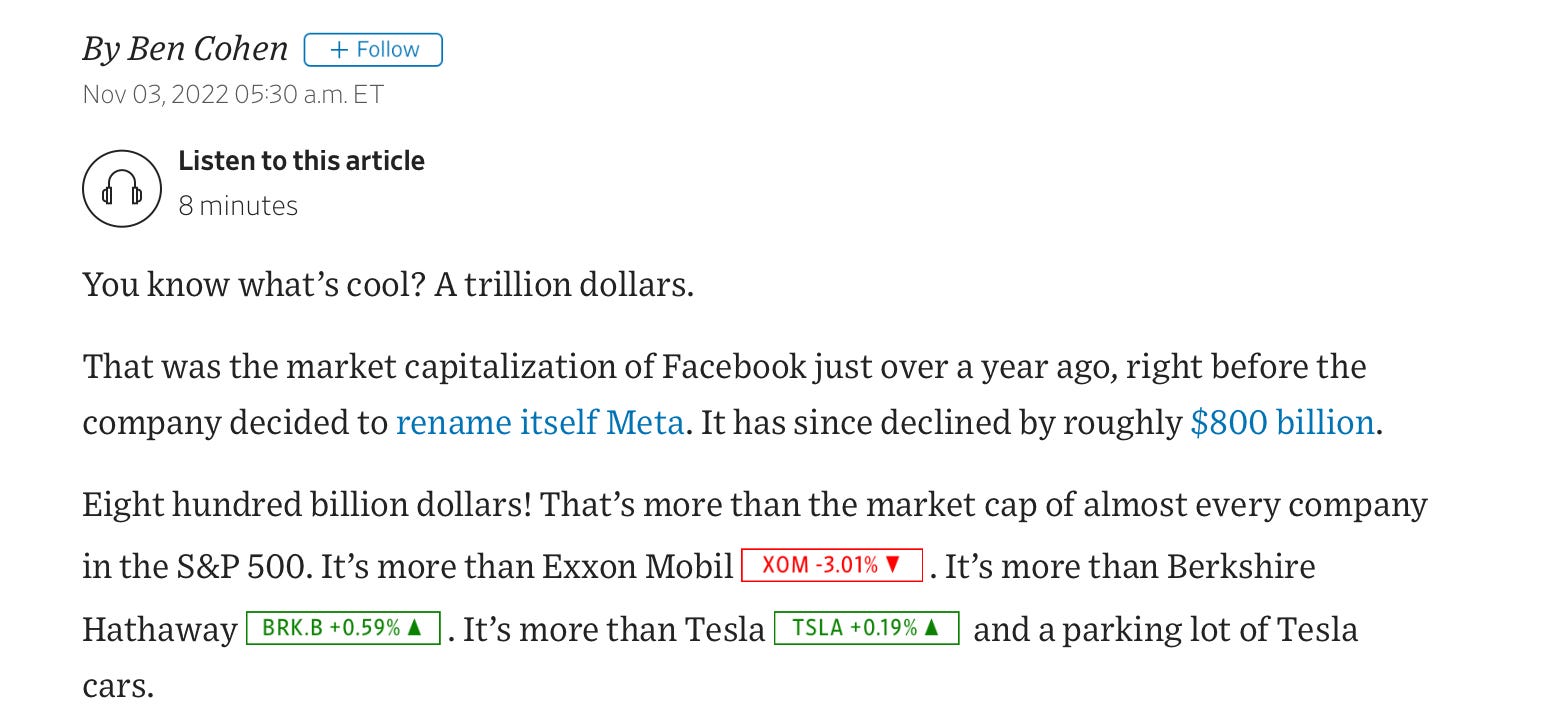

Maybe a more fair example is Meta stock, which traded down and dirty in 2022/23 and everyone was really negative about it!

Here’s an example of that negative sentiment, published in the WSJ:

Meta is worth $1.48 trillion today. I’m not sure what Ben Cohen, the journalist, has to say about that — but I guess he couldn’t look into the future (neither can I!)

Right now the narrative with Remy is i) China is buying less Cognac because of the tariffs, ii) young people aren’t drinking Cognac and iii) because Cognac sales have gone down recently they will go down in future (this is the age-old fallacy many analysts are prone to make — if something happened in the past it must happen in the future!)

The price (downwards) has driven that narrative. The pessimism is “priced into” the stock, meaning bad begets bad, and so on.

Bottoming out

Right now Remy is priced like a discount retailing selling home brewed spirits from plastic containers. Nobody is interested in a company when it’s trading like a bargain basement bottom-of-the-barrel piece of yesterday’s fish. Everybody is interested in a company when it’s on the up. Here we have a company where the only trajectory is up — because they’ve hit the bottom. We’re at max pessimism narrative, here. I like things at max pessimism. As Lord Rothschild said, buy when there’s blood on the streets… on a 5 yr basis, Remy trades around 50% of its historic multiples…

It’s well worth reading this New Yorker article about the reinvention of the storied distillery, if you haven’t already. Link.

Yes, I know this was due to technical reasons!