Santa Rally Redux

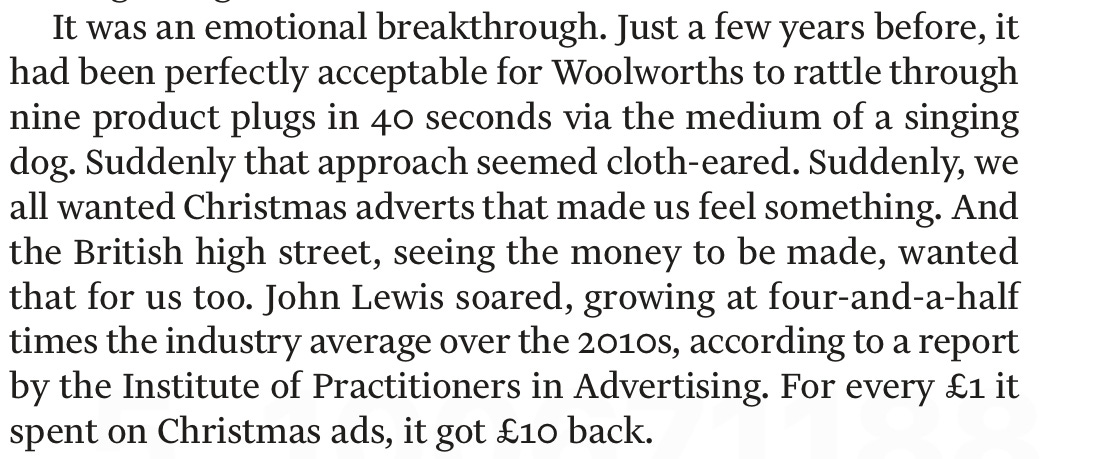

Christmas — thinking a lot about the below extract from the recent FT magazine … for every quid you spend on a heart-warming Christmas advert, John Lewis made about 10 quid back. The most merry time of the year…

Why I’m thinking about it is because it highlights that weird binary existing in the economy right now — consumers are spending, but clearly we’re in a recession (answer: people are spending but it’s on credit…). Call it “end of days” spending — or “doom spending” — when we’re living in what might be a simulation1 maybe the most rational thing to do is spend.

To recap, I think a lot of this “irrational exuberance” has its roots in COVID, because a lot of stimulus was printed and markets staged a quick comeback (that ‘‘v” shaped recovery). I also think COVID had us rethink our attitude to consumerism — if you think about it, COVID was a kind of perfect testing ground for an Amazon-everything world — order, stay at home, consume, die. That’s never really left us. Look at the revenue that Google and Meta make — the vast majority is advertising.

It’s heightened and distorted because we have a Trump presidency now, and the inherent implication from markets is that Trump = stonks go up. Trump’s administration are bitcoin maximalists, so you end up with surreal pieces of proposed legislation like the Bitcoin act.

Should we talk about that? Or more accurately, let’s call it by its full name: S.4912 - BITCOIN Act of 2024.

Under this act, the US govt will purchase one million bitcoins over five years. There are approx 21 million bitcoin, and at today’s prices that’s around a $100bn reserve.

And here’s Trump confirming he wants to do a Bitcoin strategic reserve.

It doesn’t really matter what I think about bitcoin, what matters is the selling/buying pressure. If the leader of the free world endorses bitcoin as fiat holdable by the state, then you end up with a lot of buyers.

Does it make sense? Not really. Does that matter? Not really, not while the music plays.

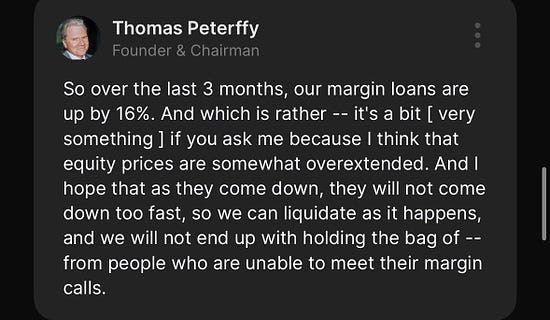

However. Here’s the founder of IBKR with reason for worry:

Am I worried? Hell yes. You also have Blue Whale selling tech stocks and Buffett with a record cash pile…

I keep thinking about dot.bomb, a book about the dot com bubble and Value America (think Amazon, but where goods were shipped directly from a supplier’s warehouse rather than one of Value America’s own). I found the book in a dusty red bin at The Warehouse (you know, back when the Warehouse used to sell discount goods and weird parallel important crap). There’s a scene where the writer talks about sitting up in bed in his boxers, watching the stock price go up and up and calling his broker to buy more. Value America failed, of course. There’s something about that exuberance — sitting in bed in your boxers watching number go up — that feels the same here. Bleary-eyed crypto investors watching their number go up, and up, and cryptocurrencies like Fartcoin having a market cap of more than $800mn.

I am sounding like a broken record here — there have been zero bubbles in history that have ended well. Zilch.

Interesting things

Every so often I remember about the flavours and fragrance sector, and then I think about Robertet, which is a French family-controlled house on the smaller side, specialising in natural fragrance. You already know I have a penchant for family owned companies, and even better when they’re old (Robertet dates back to 1850), and even better again when they have some kind of moat (in Robertet’s case, know-how and specific land resources to grow said flavours and fragrances).

Robertet trades at around 20x earnings. Compared to peers this is relatively cheap — Givaudan trades at 36x while Symrise trades at around the same multiple (I don’t like their American competitor, IFF, which is like the discount store knock-off cousin to Givaudan and Symrise).

Investors in Robertet are in good company — France’s billionaire Peugeot family recently purchased a 125mn EUR position in the company, while Fonds Stratégique de Participations recently purchased a comparable stake.

Robertet is almost wholly focused on natural raw materials (they produce over 1,000 of ‘em). There’s a bunch of inbuilt moats in there — you need supplier ingredients, relationships with farmers, land, know-how, storage facilities, etc etc. There’s a strong barrier to entry and the fact that those are natural materials that can’t be synthesised in a lab reinforces that.

French stocks trade at a discount given the govt situation. That can present opportunity. Another example is Vivendi, which is being broken up (Havas, Canal+ Hatchette, and a co holding listed and unlisted interests). Stk has done very little recently — down about 14% on the year. Shoddy back of the envelope math, here: 9.98% stake in UMG (4.4bn EUR), 23% or so of Telecom Italia (1.28bn), and a bunch of other investments. Consider also Havas as a potential acquisition target (the recent Omnicom/Interpublic merger). With a market cap of just over 8bn EUR, there’s obviously some value — rest of group minus equity investments is valued very lightly. More work to be done on that, but I love a sum-of-the-parts game…

Trump presidency, Boris Johnson existing, Elon Musk, etc…