Why I love multiples and why most of your money is made in the buying

Why I love multiples and why most of your money is made in the buying

Today’s newsletter is a (lightly) edited reply to one of my readers — I thought it would be worth sharing with you all —

Why I love multiples and why most of your money is made in the buying

By Eden Bradfield, slow learner.

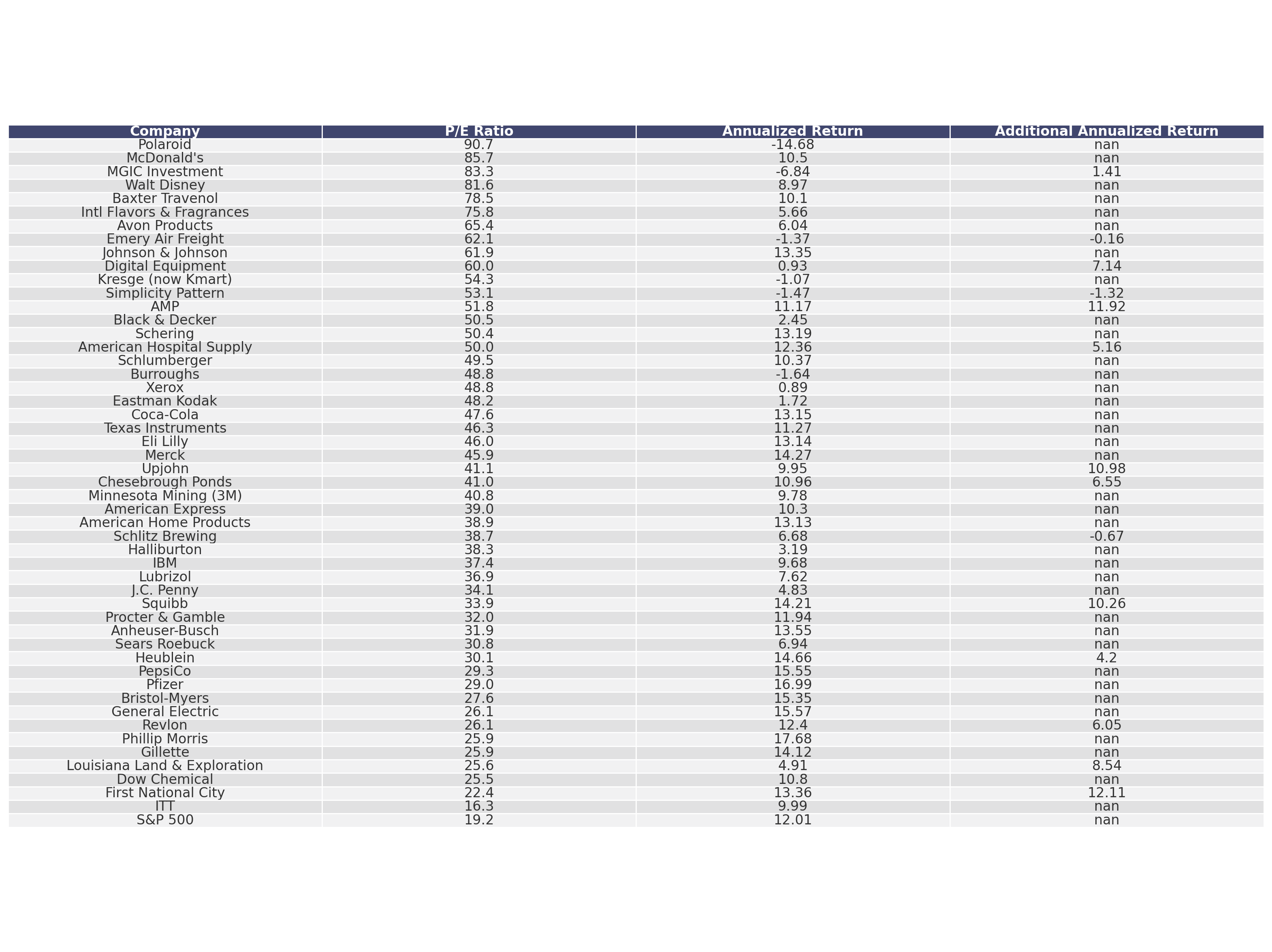

I am quite slow but I have realised re-rating is the name of the game. I had an old mentor who would always say -- you make all your money in the buying. It's true. You can buy a good company at a high multiple and not make any money. The best example of this that I can think of is the "Nifty 50" of the 60s and early 70s -- a group of stocks (50 of 'em) that exhibited high growth characteristics and often traded at astonishingly high multiples -- the average P/E ratio for a nifty 50 stock was about 42x (!!) whereas the average P/E for an S&P 500 company at the time was about 19x. See below — Nifty 50 stocks and their multiples at 19721

A lot of the companies in this motley group of stocks were great companies -- Coca-Cola, American Express, McDonald's. They still are. Yet they traded at such high multiples that, when the bear market came for them, they crashed and fell hard. See the chart below.

Prior to the bear market of '72, Nifty 50 stocks did wonderfully. They were the equivalent to your Mag 7 stocks today. Managers of money would've been questioning themselves if they weren't on that train.

Many investors would steer clear of these stocks once they had hit their low -- they are going in the wrong direction! And yet we know that this clutch of stocks has done fabulously over the last few decades.

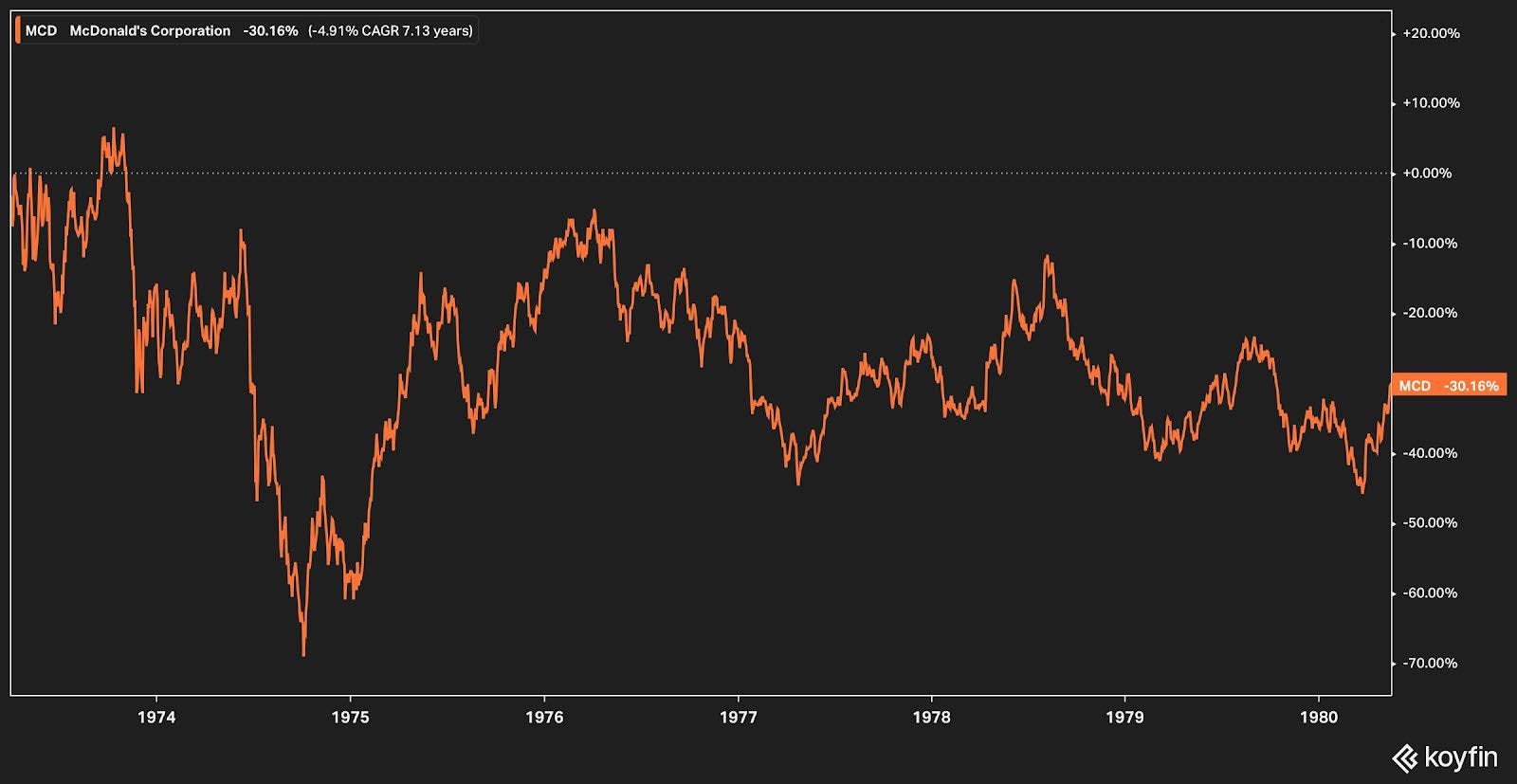

It's worth pointing out that it would have taken a long time to recoup your gains had you bought MCD around the time of its late 60s/early 70s peak, where it traded at +40x earnings (I’ll talk about that a bit later). This is in spite of it growing its EPS at a double-digit rate every year. Ditto many of the other stocks in the “Nifty 50”.

My point is twofold. You can buy a great company at a high multiple and it will take a long time to make your money back because reversion to the mean is a mathematical certainty that, like death and taxes, happens to all companies.

You can also buy a great company while it is going up (and up), but if you buy at said high multiple you risk being caught in the rally and subsequent fall. There have been many rallies over time: the railroad bubble of the 1800s, the bicycle bubble, the telecommunications bubble, etc.

If you buy a company cheaply -- i.e. when you are "catching a falling knife" -- then you need to be sure that it is a good company. A company is not its stock price. In my newsletter on Friday I gave the example of Meta, but the Nifty 50 examples above work too, as does Amazon at the dot com crash or Chipotle around the time it had the food safety scandal (or salad oil with American Express). Often temporary market panics give you an opportunity to buy cheaply -- maybe it is a scandal, or a bad quarter, or an overreaction to a news event. I don't care too much. The point is, do the fundamentals stack up?

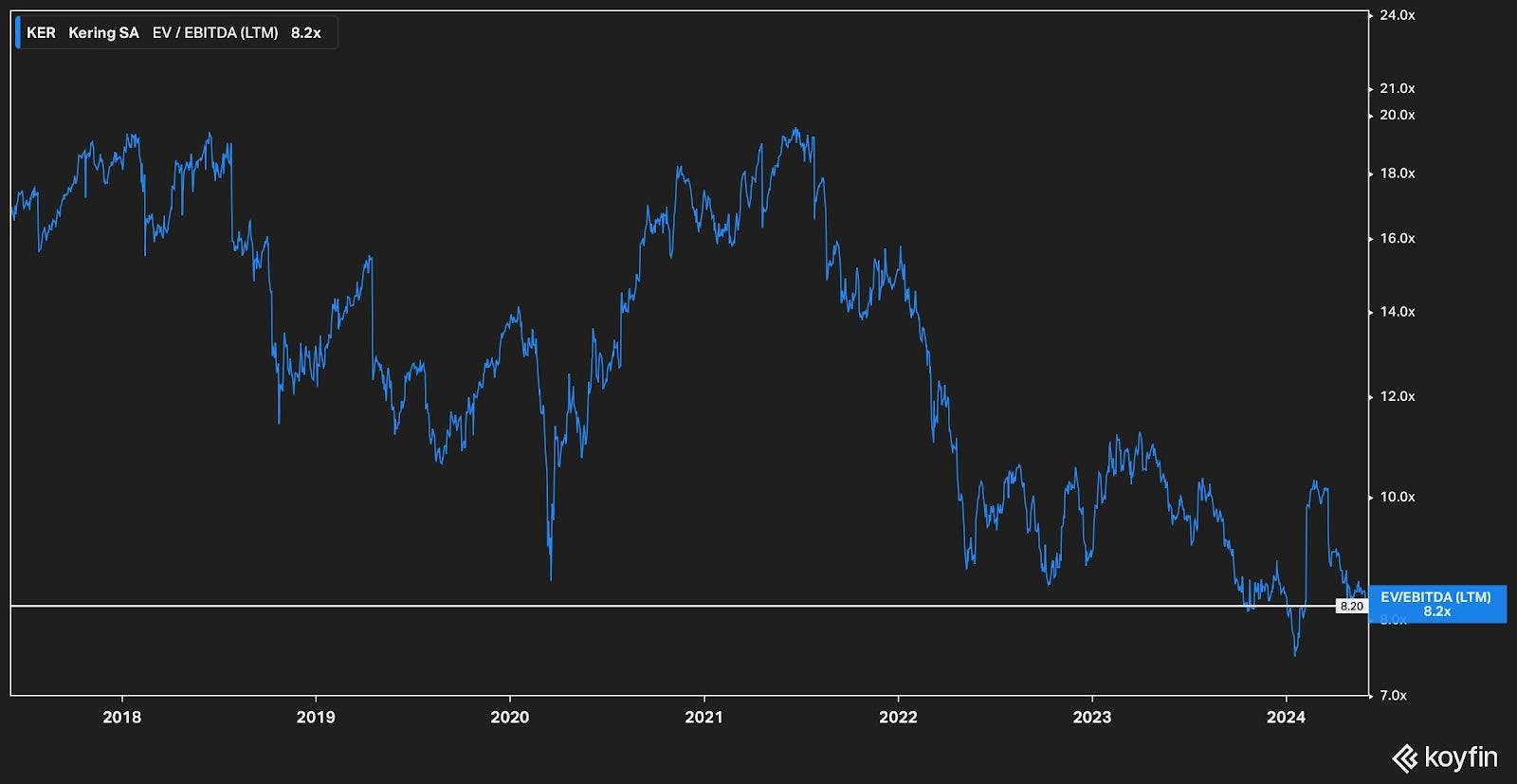

If they do then I back up the truck. An example at the moment is Kering. Kering owns Gucci, Balenciaga, Saint Laurent, and so on. It also has an enviable property portfolio. Gucci sales fell off a cliff after the previous designer left. Kering trades at 13x earnings. Not so long ago it traded at +20x earnings. Its total revenue and margins have not changed that much since it traded at 20x earnings. The market, in other words, is pricing it like a cut-price discount retailer that hawks polyester clothes in Timaru gand not a luxury retailer with significant pricing power, brands and footprint.

Finance bros are infamously bad at understanding the nuances of fashion. They mostly dress terribly, or in vests, or both. The stock is priced like Gucci will never recover, which is just dumb -- they still sell loads of clothes and bags and generate billions in revenue; in addition Kering has these smaller houses which are actually growing. The "street" doesn't quite understand that, because most analysts are not good at assessing fashion because they haven't been watching the industry for a long time and all they see is numbers — numbers are always a byproduct of the business, not the other way around.

I came up in fashion. My first break was writing a popular fashion blog, in 2009. I understand this stuff intimately. I have a demonstrable edge against a lot of the market, which is why I am buying Kering by the boatload. I've attached a graph of Kering's EV/EBITDA to show what I mean -- the last time in traded down so much as around COVID.

If you do a peer analysis you will find that comparable companies trade at +20x earnings (LVMH, Hermes, Prada, Richemont…). They command similar margins, do similar things and occupy a similar part of consumer mindshare. There is nothing particularly smart about buying Kering at this level -- I am simply waiting for reversion to the mean.

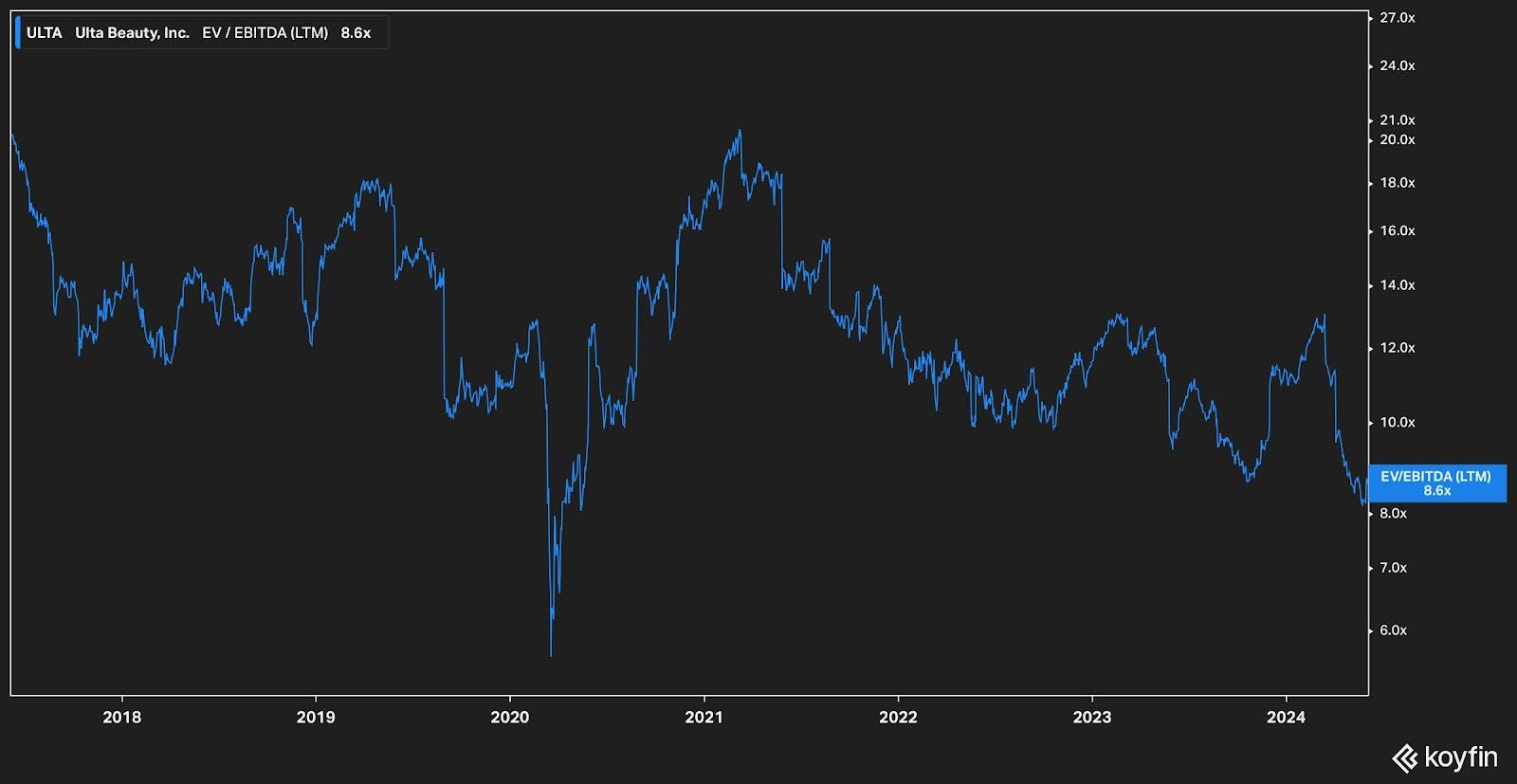

A counter-example: ULTA, which is a beauty retailer in the US. I'll use an EV/EBITDA chart for consistency.

Why am I not buying this by the boatload? It's in a similar industry and also trading around the bottom end of its multiples, right? (I’m also picking on it because it’s a current darling of FinTwit).

This is why business model is important. Ulta has very little competitive advantage. There are many Ulta outlets, all selling the same cosmetics. Their margins are at the behest of the companies they buy from. They also have intense competition, from superior operators like Sephora (Sephora, by the way, is owned by LVMH -- i.e. it has an endless supply of cash and it has obvious synergies with LVMH's beauty arm). It has an 11% net margin vs. Kering's 15%. It also has none of the advantages of brand -- Balenciaga, Saint Laurent, etc, all have natural moats around themselves -- they have a history that is hard to replicate. You aren't buying product. You are buying an idea.

This is why the model of a business matters when you buy these companies that are trading in the "wrong direction of the market". That's also why I only ever buy within my circle of competence when doing this -- I know fashion well, and I can speak to it for hours. I know little about oil or mining, so I stay out of it.

Back to McDonald's. Its peak stock price, in that Nifty 50 era, was around March 1973. If you'd bought around the top you'd still be down by 1980. See below. This is in spite of McDonald's being a fabulous business!

Prior to that, by the way, McDonald's had been on a hell of a run -- it was the growth stock de jour of the late 60s. This doesn't really matter if you buy it wrong -- as I referenced at the start, you make all your money in the buying. Multiples matter; price matters.

I know it's a hackneyed quote -- if you like burgers at $20 you're going to love them at $10 -- but it's true. If you understand the business you are buying you are going to love it at a discount.

For the large part of '21 and '22 people looked at me like I was crazy because I wasn't buying Tesla. It was the hottest stock. Now it is not. There is always a hot stock. I am not very interested in what a hot stock is. I try and buy businesses with sustainable characteristics that can operate with a competitive advantage at a good price.

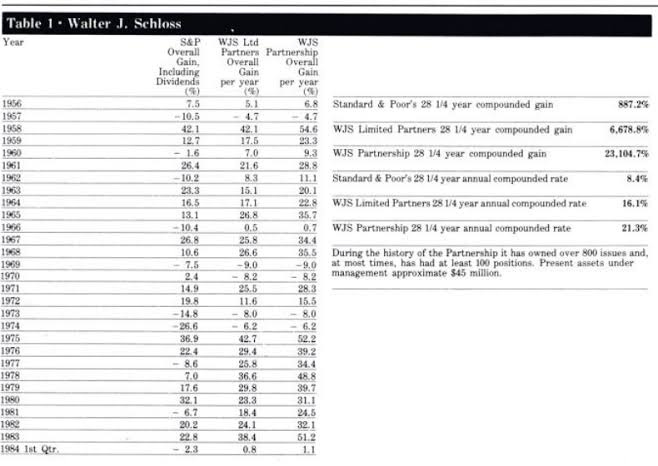

I’ve attached the record of Walter Schloss below, who famously spent most of his career buying falling knives and stocks trading at 5 - 10 year lows (he didn’t care about the fundamental franchise quality of a business as much as say, Munger). Over time he did very well. Falling knives that continue to make money and re-rate will do you well. I prefer to add in quality, because it’s how I operate — others, like Schloss, did just fine without it. The reason I show it is because I think Schloss is the most pure example of you make all your money in the buying. Take it away, Walter — his record from 1956 - 1984:

n.b — stocks with double entries were either involved in mergers or buyouts